NEWSLETTER: Oct. 10th 2018

The SEC Needs to End Its Self-Inflicted Blindness and Implement CAT ASAP

The SEC Needs to End Its Self-Inflicted Blindness and Implement CAT ASAP

The Consolidated Audit Trail (CAT) would revolutionize the SEC’s capabilities to protect investors, facilitate capital formation and promote fair and orderly capital markets – on which job creators and savers, and indeed all Americans, depend. It is no exaggeration to say that our sprawling, fragmented, nanosecond-moving equity markets live on a knife’s edge every day: will today be the day when the next “flash crash” occurs and trillions of dollars disappear for no known reason? Will the markets immediately rebound as they did in May 2010, or will the next “flash crash” ignite a global chain reaction that causes markets worldwide to plummet, undermines market confidence, or even, as some have speculated, trigger the next catastrophic global financial crash?

The CAT will be the world’s largest data repository for securities transactions, tracking billions of orders, executions, and quotes in all of the equities and options markets every day. More specifically, the CAT will collect order, cancellation, modification, and trade execution information for every trade. That information will serve two vital functions: enabling the SEC not only to reduce, manage, and better understand market disruptions and crashes, but also to identify, deter, and punish illegal manipulation and other trading abuses – all for the benefit investors and our markets.

That is what is at stake in the completion and implementation of the CAT. And yet despite repeatedly missing numerous previous deadlines, the Securities and Exchange Commission (SEC), with no notice and with no opportunity for the public to weigh in, has granted another lengthy delay to the industry to create and operate the CAT.

Almost a year ago, the SEC took the opposite approach, holding firm and refusing to grant additional time to finish this long-overdue and essential tool and database. At the time, Better Markets praised SEC Chair Clayton for standing firm in the face of industry pressure. One must wonder, then, what has changed in the intervening year. Additionally, as Better Markets pointed out in a recent letter to Chair Clayton, the SEC would be well within its authority to impose fines on CAT NMS for the constant delays and failure to deliver yet has failed to do so.

Already years overdue, the SEC simply must start meaningfully sanctioning the industry consortium tasked with building the system. That apparently is the only thing that will stop further delays in its development and implementation.

Already years overdue, the SEC simply must start meaningfully sanctioning the industry consortium tasked with building the system. That apparently is the only thing that will stop further delays in its development and implementation.

Until the CAT is fully-implemented and operational, the SEC will be blinded, leaving Main Street consumers, tens of millions of investors – importantly, including Mr. and Mrs. 401(k) – and financial markets at grave risk of a run-a-way crisis if not a full-blown meltdown. The time for the SEC to act is long overdue and the time to start imposing substantial fines and penalties is now.

New Study on CFPB Lending Oversight Shows Banks Make Better, Less Risky Loans

New Study on CFPB Lending Oversight Shows Banks Make Better, Less Risky Loans

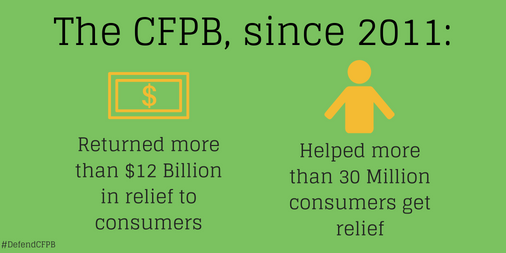

- The Consumer Financial Protection Bureau (CFPB) has been the single most successful consumer protection agency in the history of the Federal government, returning $12 billion to 30 million ripped off consumers. Because of that – because the financial institutions wanted to keep the $12 billion in their bonuses rather that repay ripped off customers – Wall Street and its allies have been relentless in making various false claims about it, including that the CFPB has increased costs, created uncertainty, and over-reached in its oversight of financial institutions.

A new staff report from the Federal Reserve Bank of New York, Does CFPB Oversight Crimp Credit?, provides new evidence on the CFPB’s supervisory and enforcement activities and shows that the negative impact on banks has been virtually nonexistent while the overall credit health of borrowers has improved.

The paper specifically looked at consumer lending activities at commercial banks and savings banks with total assets between $1 billion and $25 billion and found that the effect of CFPB oversight on mortgage loan volume was quite small and “not statistically different from zero.” More specifically the paper stated:

- “In other words, there is no evidence that being subject to CFPB supervision and enforcement has led to lower mortgage lending for affected banks.”

Additionally, the researchers did find that there was some impact on the composition of lending, with a 6% decrease in Federal Housing Administration-backed loans and some decrease in lending to borrowers that are a higher credit risk. In other words, CFPB oversight is doing exactly what it was intended to do: prodding banks to improve the quality of loans being made with essentially no adverse cost impact on lenders.

Additionally, the researchers did find that there was some impact on the composition of lending, with a 6% decrease in Federal Housing Administration-backed loans and some decrease in lending to borrowers that are a higher credit risk. In other words, CFPB oversight is doing exactly what it was intended to do: prodding banks to improve the quality of loans being made with essentially no adverse cost impact on lenders.

What You Think You Know About TARP and Wall Street’s Biggest Banks Is Wrong

What You Think You Know About TARP and Wall Street’s Biggest Banks Is Wrong

Ten years ago this Saturday, on October 13, 2008, the CEOs of the biggest banks in the U.S. were summoned to a meeting at the Treasury Department where they all received taxpayer bailouts in the form of TARP (Troubled Asset Relief Program) money from the Federal government. The money was being given to the banks, we were told, to buy up bad mortgages from the banks and modify them to help borrowers, to stimulate lending to small businesses, and other activities meant to inject capital and confidence into the reeling financial system

Here’s the catch: The mythology of TARP is wrong.

Myth #1: TARP funds were to be used to help consumers with small business loans, mortgage relief and other assistance.

- In the months following the bailout, lending among the biggest banks actually went down. The largest decrease in lending also came from the biggest recipient of bailout money, Citigroup, which had a 3.1 percent drop in lending. Further, the inspector general for the bailout found that lending among the nine biggest TARP recipients “did not, in fact, increase.”

Myth #2: Some banks were forced to take TARP money even though they didn’t really need the help.

- The answer to the question, “Why didn’t the banks lend out the TARP money they received?” can be found in the fact that the banks needed it themselves to maintain their own financial health. In testimony before the Financial Crisis Inquiry Commission, then-Fed Chair Ben Bernanke admitted that 12 of the 13 most prominent financial companies in America were on the brink of failure during the time of the initial bailouts.

Myth #3: The Federal government “made money” on TARP.

- The Federal government was repaid the TARP funds but didn’t make money on the bailouts. According to the latest Treasury report to Congress, cumulative TARP collections exceeded the $440 billion in disbursements by just $2.4 billion, which is a ½ percent total return. Contrast that to Warren Buffett’s returns on his crisis investments: more than 70% (as we detailed in our Costs of the Crisis Report at pages 66-69). Most importantly, none of the money returned to taxpayers were on a risk-adjusted basis, which is the way only way returns can be evaluated and who Wall Street judges every loan and investment. The persistent myth that “the bailouts made money” has allowed the mega-banks to claim that since no money was lost, we no longer need the protections put in place by the Dodd-Frank Act, despite the vast damage the crisis inflicted on the American people.