With Red Lights Flashing Danger, Where Are the Adults in Finance?

With Red Lights Flashing Danger, Where Are the Adults in Finance?

It seems almost everyone in finance is cheering on the deregulation frenzy in Washington and the demise of consumer protection and enforcement in the financial markets. Given that an historic crash happened just ten years ago and the too-frequent predatory conduct in the industry still hasn’t abated, this is an irresponsible, knowing dereliction of duty by bankers and public officials who know better.

Rules and enforcement not only protect consumers, investors and taxpayers, but also financial markets and the financial industry itself. They not only prevent catastrophic financial crashes, but also direct financial activities toward the real economy while nurturing and maintaining investor and public confidence in our markets. That trust is the foundation upon which our markets are built and work, becoming the envy of the world.

While rules and enforcement are essential in normal times, they take on heightened importance now when we are nine years in to the boom phase of the business cycle; when leverage is breaking records while interest rates are rising; when the punch bowl was just spiked with $2 trillion in stimulus; and, when the unprecedented Fed actions over the last ten years are going to be unwound by equally unprecedented actions.

Making matters worse, enforcement of the rules has dropped precipitously, which is equally bad news for everyone, as an astute market observer, Brooke Masters at the Financial Times, noted in a column entitled “Wall Street Must Suppress its Delight at Eric Schneiderman’s Fall”:

“History suggests that financial abuses tend to multiply at the end of an economic boom, as market participants try to keep the good news flowing. We are in the eighth year of an upcycle, yet President Donald Trump’s administration is loosening the rules on banks, and his choice as US Attorney for the Southern District — another vital financial crime watchdog — is untested.

“History suggests that financial abuses tend to multiply at the end of an economic boom, as market participants try to keep the good news flowing. We are in the eighth year of an upcycle, yet President Donald Trump’s administration is loosening the rules on banks, and his choice as US Attorney for the Southern District — another vital financial crime watchdog — is untested.

“Mr Schneiderman did the right thing by resigning. But his disappearance leaves us without a determined cop on Wall Street at a time when investors are particularly vulnerable. That cannot be good for anyone.”

With laws and rules being weakened and not enforced, this is precisely when the adults in finance need to reflect on the unacknowledged wisdom of former Citigroup’s CEO Chuck Prince’s infamous quote:

With laws and rules being weakened and not enforced, this is precisely when the adults in finance need to reflect on the unacknowledged wisdom of former Citigroup’s CEO Chuck Prince’s infamous quote:

“As long as the music is playing, you’ve gotta get up and dance . . . .”

Translation: once financial firms (particularly the market leading too-big-to-fail financial firms on Wall Street) start to engage in high-risk, high return activities, the competitive pressures due to rising revenues, profits, bonuses, and stock prices will be irresistible and push them all into a competitive spiral, however irresponsible or unwise.

That’s exactly why former Morgan Stanley’s CEO, John Mack, said after the crash:

That’s exactly why former Morgan Stanley’s CEO, John Mack, said after the crash:

“[w]e cannot control ourselves. You [lawmakers and regulators] have to step in and control the Street. Regulators? We just love them.”

Yet, at this time of frothy vulnerability with risks multiplying, the opposite is happening. Financial deregulation in the legislative, regulatory and judicial arenas is proceeding apace, as if none of that matters. As former Fed Vice Chair Stanley Fischer stated:

“One can understand the political dynamics of this thing, but one cannot understand why grown, intelligent people reach the conclusion that [you should] get rid of all the things that you have put in place in the last 10 years.”

Fortunately, there are a few public officials speaking out and taking a stand against this often-mindless deregulation. For example, Fed Governor Lael Brainard recently talked about considering increasing capital and other so-called “counter-cyclical” buffers. She also voted against the Fed’s recent proposal to lower capital and weaken the leverage ratio. This was “the only dissent among 315 Fed board votes on record since 2012.” Given the enormous pressure at the Fed for consensus, that takes real courage. Similarly, under the leadership of Chairman Marty Gruenberg, the FDIC refused to go along with the Fed and OCC in its proposal to reduce capital, even in the face of unwarranted public criticism.

Fortunately, there are a few public officials speaking out and taking a stand against this often-mindless deregulation. For example, Fed Governor Lael Brainard recently talked about considering increasing capital and other so-called “counter-cyclical” buffers. She also voted against the Fed’s recent proposal to lower capital and weaken the leverage ratio. This was “the only dissent among 315 Fed board votes on record since 2012.” Given the enormous pressure at the Fed for consensus, that takes real courage. Similarly, under the leadership of Chairman Marty Gruenberg, the FDIC refused to go along with the Fed and OCC in its proposal to reduce capital, even in the face of unwarranted public criticism.

We applaud both Gov. Brainard and Chairman Gruenberg for speaking out and standing up, but they shouldn’t be so alone. Others, Democrats, Republicans and financial industry leaders, simply must speak up and act in the greater good, not only of finance but of the country.

We applaud both Gov. Brainard and Chairman Gruenberg for speaking out and standing up, but they shouldn’t be so alone. Others, Democrats, Republicans and financial industry leaders, simply must speak up and act in the greater good, not only of finance but of the country.

Flash Crash Anniversary a Reminder of Why Regulators Need New Tools Like CAT to Protect Investors, the Financial System and the Economy

Flash Crash Anniversary a Reminder of Why Regulators Need New Tools Like CAT to Protect Investors, the Financial System and the Economy

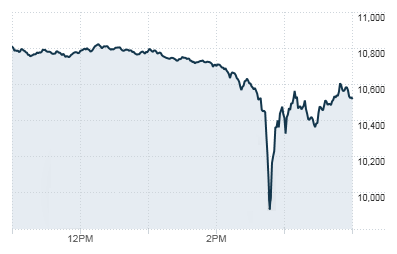

This past Sunday marked the 8th anniversary of the “Flash Crash,” when nearly one trillion dollars of stock market value was inexplicably wiped out in a matter of minutes. This confidence-shattering event happened over just 18 minutes and caused some stocks plummet to $1 per share and others to skyrocket to more than $100,000 per share. Yet, it took regulators many months to reconstruct what happened. Reports were issued, hearings were held, but still many questions remain about what led to and what happened during the “Flash Crash.”

That’s why the Securities and Exchange Commission (SEC) took action to create better tools to gather and analyze data, to better understand the genesis of market disruptions, and, if possible, prevent these events. The key tool to be created was called the “consolidated audit trail” or “CAT”. The CAT will serve two vital functions, enabling the SEC not only to reduce, manage, and better understand market disruptions and crashes, but also to identify, deter, and punish illegal manipulations and other trading abuses – ultimately all in the name of protecting investors and our markets.

But the CAT has been beset by bad decisions and delays. Today, eight years after the Flash Crash, the CAT still doesn’t exist. It’s development is paralyzed under the weight of the competing industry group unable and unwilling to take the necessary action to make the CAT a reality. The most recent example was a missed deadline last November when the CAT was supposed to begin collecting data. Now, more than seven months after that deadline, the CAT remains non-existent and non-functioning. Put differently, the SEC is almost as blind to market events as it was eight years ago when the Flash Crash stunned everyone.

It is unacceptable that the CAT system remains unfinished and unimplemented. Similar crashes will certainly happen again and it is in the interest of policymakers and all responsible industry participants to arm regulators with effective tools against such events. Until the CAT is operating, the SEC will remain blindfolded in its market surveillance activities, leaving Main Street consumers, millions of investors, and financial markets in harm’s way.

Mulvaney’s Latest Maneuver to Weaken the CFPB and Erode Consumer Protections

Mulvaney’s Latest Maneuver to Weaken the CFPB and Erode Consumer Protections

Along with many, many others, we took note of CFPB acting director Mick Mulvaney’s recent remarks to the American Bankers Association, but not for the same reason. There’s no denying that his comments about the preferential treatment given to lobbyists that had contributed to his campaign were outrageous and epitomize the Washington swamp. However, those comments have overshadowed yet another action by Mulvaney to further weaken the CFPB and the critical protections it provides American consumers by eliminating public access to the Bureau’s consumer complaint database.

While the first remark received a lot of attention, the second will prove to be more harmful to Main Street consumers.

If acting director Mulvaney is successful in removing the public’s access to the consumer complaint portal, it will mean consumers will no longer be able to see if others have also been ripped off in the same way by the same firm. This means you, your family, and your friends will be left in the dark and unable to see complaints registered by other Main Street consumers. This decreases accountability at the CFPB and increases the possibility that millions of other consumers will unwittingly take their business to a bad actor because they don’t know any better and unfortunately won’t have the benefit of this shared source of vital consumer information.

As noted in a recent Bloomberg editorial, open access to the database has been beneficial to the firms themselves. Once a complaint is publicly posted, it is sent along to the company which has 15 days to respond. This has resulted in consumers receiving a quick response from the company 97% of the time and a positive resolution for the consumer about 80% of the time. Furthermore, the database compels the CFPB to act and also provides a gigantic set of data for journalists and researchers to evaluate and assess how both industry and the bureau are performing.

This is not the first time Mulvaney has taken a step towards protecting financial predators and away from the Main Street consumers who desperately need as much help as possible. In fact, in the 5+ months since President Trump appointed Mulvaney as acting director of the CFPB, Mulvaney has made 20 anti-consumer moves, all of which have been tracked on our blog: “Putting the CON in Consumer Financial Protection Bureau.”

A New, Untested, and Dangerous Weapon Against Health and Safety Rules

A New, Untested, and Dangerous Weapon Against Health and Safety Rules

In an effort to bring a new weapon to their fight, opponents of common sense regulations of all types are seeking to use the Congressional Review Act in a new, untested, and dangerous way that could potentially threaten rules going back to the Clinton administration.

Recall that at the end of last year, Senator Pat Toomey (R-PA) sought and successfully obtained a decision from the General Accounting Office regarding the CFPB’s auto lending guidance, asking if it qualified as a rule under the Congressional Review Act. The GAO said that it did. The law requires that rules be submitted to Congress for their potential disapproval so it stands to reason that something that was issued as guidance and not a rule would not have been sent to Capitol Hill. Additionally, under the Congressional Review Act rules could be undone with a simple majority vote, allowing the Senate to avoid the need to overcome the 60-vote threshold of a filibuster.

Now opponents of all manner of protections, ranging from financial rules to protections for workers, consumers, minorities, investors and the environment are threatened. As a result, actions going back to the Clinton years could theoretically now be undone.

This dangerous development reflects the prevailing view that rules regardless of merit or necessity are bad or, as former Congressman Barney Frank quipped, “a rule is guilty until proven innocent.” That unfortunately now means that protections that consumers and hardworking families rely on as they live their lives, seek to put food on the table, a roof over their family’s head, save for a college education or a safe and secure retirement may be overturned, leaving them vulnerable once again.