THIS WEEK IN FINANCIAL CRISIS HISTORY:

- September 7th, 2008 – In an historic and unprecedented move, the U.S. Government places Fannie Mae and Freddie Mac into “conservatorship” (meaning the US Government took over control of the two mortgage giants) in an effort to stabilize the housing market.

- September 11th, 2008 – Lehman Brothers puts itself up for sale in effort to save itself from bankruptcy

- September 12th, 2008 – NY Fed meets to try and save Lehman Brothers

- September 15th, 2008 – Bank of America announces it will buy Merrill Lynch

- September 15th, 2008 – Lehman Brothers files for bankruptcy

A Potential Supreme Court Justice Kavanaugh: Good for Corporations, Bad for Your Wallet

A Potential Supreme Court Justice Kavanaugh: Good for Corporations, Bad for Your Wallet

Coinciding with Brett Kavanaugh’s Supreme Court confirmation hearing, Better Markets released a detailed report, “A Supreme Court Justice Kavanaugh: Good for Corporations, Bad for Your Wallet” examining often overlooked but hugely important cases focused on economic and financial issues. Simply stated, if you care about what’s in your wallet, the report shows you should be very worried if Judge Kavanaugh becomes Justice Kavanaugh. Anyone who gets a paycheck, has a savings or checking account, uses a credit card or debit card, or conducts financial transactions of any shape or form—in other words, every single American—should care about how a Justice Kavanaugh would rule on critical financial issues that directly impact every American family.

That’s because the report finds that Judge Kavanaugh has a long record of and can likely be expected to cut back on investor protections and limit regulatory agencies from fulfilling their missions. Overall, a Justice Kavanaugh can be expected to favor business interests over American consumers, investors and workers.

More specifically, the report examines key upcoming Supreme Court cases, analyzes Judge Kavanaugh’s record as a judge on the D.C. Circuit in economic and financial cases, and surveys some of the most important legal holdings in the financial arena, showing the profound impact that these cases have on every American and their financial well-being.

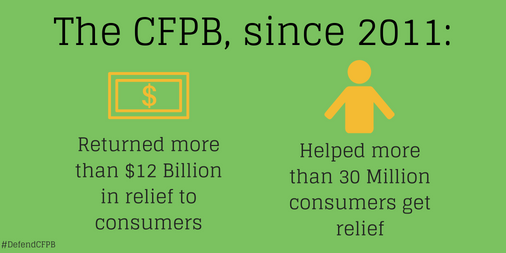

Judge Kavanaugh’s rulings reflect a deep hostility toward independent regulatory agencies that exist to protect the health, safety, welfare, and financial well-being of all Americans. For instance, instead of siding with consumers ripped off by financial predators, Judge Kavanaugh believes the Consumer Financial Protection Bureau threatens the individual liberty of Americans. We have a hard time understanding how an agency that has returned more than $12 billion to 25 million ripped off Americans is a threat to their liberty. Frankly, having $12 billion taken from the pockets of Americas families and fraudulently moved into bankers’ bonuses is a threat to American’s economic security, savings and financial well-being.

Judge Kavanaugh’s rulings reflect a deep hostility toward independent regulatory agencies that exist to protect the health, safety, welfare, and financial well-being of all Americans. For instance, instead of siding with consumers ripped off by financial predators, Judge Kavanaugh believes the Consumer Financial Protection Bureau threatens the individual liberty of Americans. We have a hard time understanding how an agency that has returned more than $12 billion to 25 million ripped off Americans is a threat to their liberty. Frankly, having $12 billion taken from the pockets of Americas families and fraudulently moved into bankers’ bonuses is a threat to American’s economic security, savings and financial well-being.

He also narrowly interprets the federal securities laws that prohibit fraud, going so far as to take to task the Securities and Exchange Commission for trying to apply those provisions broadly to protect investors. And he can be expected to chip away at, if not work to abolish, a bedrock principle known as the Chevron doctrine that requires courts to defer to experts at the financial protection agencies.

Looking ahead to the upcoming Supreme Court term that begins on October 1, the Court’s docket includes a number of cases that will impact the financial security of every American. For example, one cases might well determine if ripped-off consumers will be forced into industry-biased mandatory arbitration or will be able to go court like all other Americans. The Court will also hear cases that will influence the extent to which states can protect consumers without being pre-empted by federal law. Finally, the Court will also be hearing cases that could potentially eliminate anti-fraud protections for investors and also limit their ability to get meaningful compensation.

The full report can be found here on the Better Markets website.

Better Markets’ Wins One For Transparency, Democracy and Public Involvement

Better Markets’ Wins One For Transparency, Democracy and Public Involvement

The Dodd Frank financial reform and consumer protection act banned speculative proprietary trading by what is called the “Volcker Rule” named after former famed Fed Chairman Paul Volcker. That prohibition stopped Wall Street’s biggest banks from betting with taxpayer backed deposits and limited their subsidized unfair competition. The Volcker Rule was one of the most important financial reforms to be enacted in the ashes of the 2008 crash, not only because of those limitations, but also because it curbed the gambling culture that had infected too much of the banking industry.

Earlier this year, the federal agencies charged with overseeing and enforcing the Volcker Rule proposed weakening it, but only provided the public with 60 days to comment. Give how important the ban is to protecting Main Street from Wall Street, that was a grossly insufficient period for public comment. Making it worse, the regulators laughably claimed they were merely “simplifying” the rule, but their proposal ran 689 pages and included 342 specific questions on numerous technical concepts and provisions. While 60 days may be plenty of time for Wall Street’s unlimited resources and its army of lobbyists, it was grossly inadequate for the public and public interest groups.

![]() In response, Better Markets, joined by Public Citizen, Americans for Financial Reform, and the Center for American Progress, requested an extension to the comment period to provide the public with a more meaningful opportunity to analyze, evaluate and respond to this very consequential proposal. Just this past week, we are happy to report, federal regulators announced that they had extended the comment period for an additional 30 days.

In response, Better Markets, joined by Public Citizen, Americans for Financial Reform, and the Center for American Progress, requested an extension to the comment period to provide the public with a more meaningful opportunity to analyze, evaluate and respond to this very consequential proposal. Just this past week, we are happy to report, federal regulators announced that they had extended the comment period for an additional 30 days.

While still insufficient, the extension is essential given that it was only ten years ago that the American people paid a catastrophic price for Wall Street’s reckless, bonus-driven speculation and trading. That is what the Volcker Rule was directly aimed at and the financial regulators must get the proposed changes to the Volcker Rule right or it will be those same American families who will once again end up paying the price to bailout Wall Street’s biggest banks.

Mariana Mazzucato’s New Must-Read Book: “The Value of Everything: Making and Taking in the Global Economy”

Mariana Mazzucato’s New Must-Read Book: “The Value of Everything: Making and Taking in the Global Economy”

Economist and author Mariana Mazzucato has a new book out: “The Value of Everything: Making and Taking in the Global Economy.”

The book makes the argument that modern capitalism is confusing rents with profits, value extraction with value creation, and that this confusion is a key driver of rising inequality, and falling innovation. It does so by reviewing the evolution of the concept of value in economic theory, and how the term has been used and abused in different areas, from how drug prices are set (value based pricing), how companies are run (maximizing shareholder value), the way public data has become a private good, and the way governments have been captured in the process.

Resolving these questions, she writes, are key if we are to replace the current system with a type of capitalism that is more sustainable, more reciprocal, and that ultimately works for us all.

You can read more reviews about the book here.

She is also doing a number of book events that we encourage you to attend, including in DC today, New York tomorrow and San Francisco on Thursday. You can find the info on the events on her home page under US Launch Events.

The 2008 Financial Crisis and the Crisis That Lurks Around the Corner

The 2008 Financial Crisis and the Crisis That Lurks Around the Corner

As the retrospectives precipitated by the 10th Anniversary of the collapse of Lehman Brothers roll in, a recent New York Times editorial stands out: “Inviting the Next Financial Crisis.” It looked at the 2008 financial crisis, how we’ve made the financial system safer and more secure with the Dodd-Frank Act and other efforts in the wake of the crisis, and how, tragically, the Trump administration and its financial (de)regulators are undoing much of that progress.

If you don’t have time to read the entire editorial, here are the highlights:

On the progress we’ve made and the dangers of another crisis that lurk around the crner:

“The economy has come a long way from the dark days of 2008, when the collapse of Lehman Brothers and the bailout of big banks led to worldwide economic disaster. For much of the last decade, the economy has been growing and the stock market has been rising. But this steady climb is lulling bankers, lawmakers and regulators into repeating mistakes that contributed to that crisis and cost millions of people their jobs, homes and savings.”

On the Dodd-Frank Act:

On the Dodd-Frank Act:

“Congress enacted the Dodd-Frank law, imposing tighter regulations on financial institutions and limiting their ability to take bet-the-farm risks with borrowed money. The law helped instill confidence in banks that had squandered their credibility by blowing billions on dubiously engineered investments that few understood and fewer could explain in plain English. It also created the Consumer Financial Protection Bureau, which defended consumers from predatory businesses.”

On the lingering damage the crisis did to the economy:

“The financial system and economy are clearly on much firmer ground than they were a decade ago. Wages are barely keeping up with inflation, but the unemployment rate, which climbed as high as 10 percent, has fallen to 3.9 percent.”

“Yet the economy has still not fully recovered. The per capita gross domestic product of the United States is about $70,000 smaller over the average person’s lifetime than it would have been had the economy stayed on the trajectory it had been on before the crisis, according to a recent analysis …The authors of that report…conclude that the economy is “unlikely to regain” that lost ground, a stunning acknowledgment of the permanent and significant costs of avoidable financial crises.”

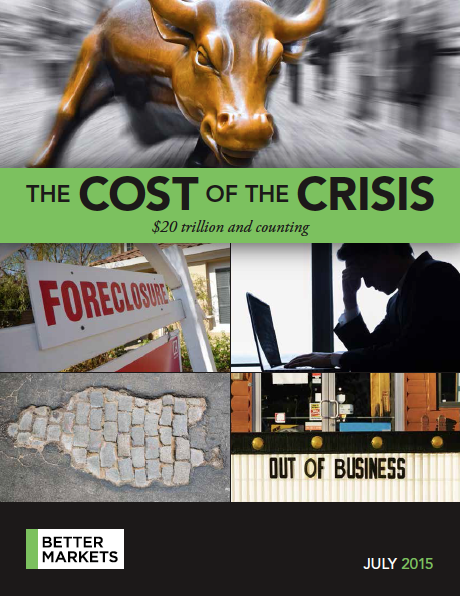

We wrote about the San Francisco Fed report in an op-ed in the Hill and how it confirmed our earlier study from 2015 that found a similar cost of the crisis, $20 trillion or $170,00 for every man, woman, and child in America.

We wrote about the San Francisco Fed report in an op-ed in the Hill and how it confirmed our earlier study from 2015 that found a similar cost of the crisis, $20 trillion or $170,00 for every man, woman, and child in America.

Given how costly the crisis was, and how expensive the next crisis is likely to be, it shows just how important financial regulation is to protecting Main Street consumers & investors and middle-class families livelihood. Yet…

“Lawmakers and the administration, and even the Federal Reserve, which should know better, are also sowing the seeds for another crisis by unraveling the financial regulations put in place in the last 10 years. In May, Congress voted to roll back parts of the Dodd-Frank law by exempting banks with assets of up to $250 billion, up from $50 billion, from stricter federal oversight. This was supposedly done to help smaller, community banks, but the change was so sweeping that it would leave fewer than 10 big banks under the kind of supervision many independent experts concluded was necessary after the crisis.

“The speed with which officials are moving to undo financial regulations is stunning to economists who remember their history. “The last time we regulated in the 1930s, it took us 30 or 40 years to take off those regulations,” said Raghuram Rajan, an economist at the University of Chicago and former governor of the Reserve Bank of India. “This time we are doing it in 10 years.”

“The speed with which officials are moving to undo financial regulations is stunning to economists who remember their history. “The last time we regulated in the 1930s, it took us 30 or 40 years to take off those regulations,” said Raghuram Rajan, an economist at the University of Chicago and former governor of the Reserve Bank of India. “This time we are doing it in 10 years.”

“And the regulations that were dismantled and eliminated could have helped prevent or reduce the severity of the last crash. Mr. Rajan, who was prescient in warning about the last crisis, said it’s unwise to deregulate now because businesses and individuals have borrowed a lot of money in recent years in the United States and other countries, raising the risks of economic problems down the road.

You can read the entire editorial here.