![]()

Fighting to give Americans the trusted retirement security advice they expect and deserve: The Department of Labor’s best interest standard is a common sense rule merely requiring brokers and other financial advisers to act in their clients’ best interest rather than their own personal interests when providing retirement investment advice. It would help those saving for retirement get the most out of these savings and help combat the retirement crisis we’re seeing in America.

Better Markets President and CEO Dennis Kelleher testified in favor of the rule during a House Education and the Workforce Committee hearing this week examining the proposal. Along with Labor Secretary Tom Perez, Mr. Kelleher provided a critical balance to the industry’s continued misinformation campaign designed to weaken this rule and prevent it from moving forward. As Mr. Kelleher told the Committee in his must-read opening statement:

“The industry’s complaints boil down to a false choice: either brokers’ get to put their interests above their clients’ best interests, or they won’t serve those clients at all. But the real choice is this: Let the DOL act to protect 100 million workers and retirees across this country, or side with the brokers and other advisers who want to continue putting their interests ahead of their clients’. That’s the real choice. If some brokers don’t want to do that or feel that they can’t make enough money doing that, then there are plenty of retirement investment advisors who will be more than willing to put the clients’ interests first. Frankly, there are tens of thousands of advisers doing that right now all across the country.”

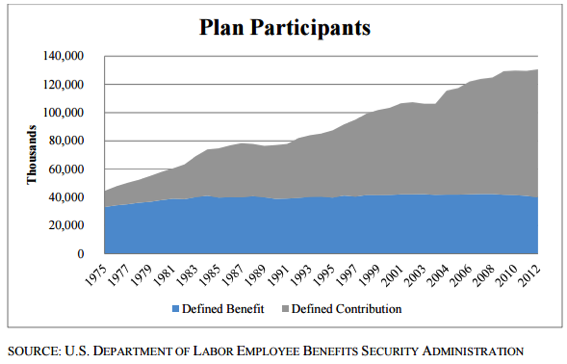

In his written testimony, Mr. Kelleher detailed how loopholes in the old rule are especially damaging in light of dramatic changes in the retirement landscape. Forty years ago, in 1975, the vast majority of all workers – 74 percent – were in large defined benefit plans. Companies like General Motors, with sophisticated investment management staff, invested on behalf of all their workers, spreading risk and reward from the market so that all employees would be assured of a comfortable retirement.

At that time, 33 million individuals participated in these plans, while only 11 million workers took part in defined-contribution plans. Individual retirement accounts (IRAs) had only just been created in 1974, and 401(k) plans were not yet in existence.

But the times have changed dramatically. As of 2012, 90 million people, or more than two-thirds of workers with retirement plans, now have defined contribution plans and are expected to manage their investments and weather the ups and downs of the market individually. The growth of these plans in the past forty years stands in stark contrast to the number of participants in defined benefit plans, which has remained flat since 1975.

This monumental shift means that Americans are forced to invest their retirement assets on their own and bear the consequences of those investment decisions. The challenge is more and more daunting, as financial products become more varied and complex. As Americans turn to brokers and other advisers to help them make these complicated and important decisions, DOL’s best interest rule will help ensure they’re getting the unbiased guidance they expect and deserve from trusted advisers.

You can read Mr. Kelleher’s written testimony here. Stay informed: Go to SaveOurRetirement.org to learn more about this issue. Stay engaged: Follow us on Twitter and Facebook for the latest news.

Judge rightfully denies AIG’s former CEO’s attempt to take $40 billion more from taxpayers, but AIG appeals: The lawsuit by AIG shareholders seeking $40 billion more from U.S. taxpayers shows once again that Wall Street greed knows no limits. The judge in the case resoundingly rejected their claim for damages this week, correctly finding that AIG stockholders did not suffer. In fact, they received a windfall solely due to being bailed-out by U.S. taxpayers. It was a stunning loss for AIG’s former CEO and the already bailed-out shareholders.

Soon after the verdict, former AIG CEO Hank Greenberg made clear he’ll continue trying to get even more taxpayer money. A statement of appeal was quickly filed that explicitly admits he is going after “billions of dollars” more of U.S. “citizens’ money.” He states he is appealing so that he can move U.S. “citizen’s money” into the pockets of AIG’s shareholders who were saved and bailed out by those very “citizens,” proving the old adage no good deed goes unpunished.

AIG shareholders wouldn’t exist today and wouldn’t own almost $90 billion in stock today but for the generosity of those very “citizens.” U.S. taxpayers were victimized here by AIG when it acted recklessly, precipitated the crash of the financial system, took a $185 billion bailout, and then gave bonuses to some of the very same people who irresponsibly sold the derivatives that blew up the company.

That type of recklessness by Wall Street shows that the unfinished job of financial reform must be completed. Hopefully, the federal appeal court will correctly determine that there would be no justice if U.S. citizens were required to give those shareholders another undeserved windfall.

New report highlights the need to restore the rule of law in our markets to protect public and investor confidence: Last week, British authorities published their long-awaited “Fair and Effective Markets Review.” The report was commissioned in response to ever mounting evidence of confidence-eroding market manipulation and abuse. It is noteworthy in several areas:

- First, it slams the depth and breath of cultural failing within the banking industry. Contrary to what the lobbyists would have one believe, misconduct was not the work of “a few bad apples.” The entire barrel was rotten.

- Second, the report highlights the failings of fines as a deterrent and the urgent need for personal accountability.

- Third, the UK recognizes that although global markets need a global regulatory response, the UK will not wait for international agreement before pressing reforms at home. Instead, the Bank of England’s Governor Carney will use his position as Chair of the Financial Stability Board to encourage other nations to embrace the essence of the new UK approach.

Whether the recommendations will be fully enacted and when remains to be seen. And, once again, a large degree of needed change is left to be voluntarily implemented by the banks themselves, i.e., self-regulation. Though the report warns that, “If firms and their staff fail to take this opportunity, more restrictive regulation is inevitable,” it is surprising and a little disturbing given the findings of more than a decade of broad based failures from the executive suites to the trading floors. Official recognition that personal accountability counts and must be restored is long overdue, but that alone simply won’t be enough and, as we have seen, will break down when the go-go years return as they inevitably will.

Hard and firm rules that are aggressively enforced – especially against individuals including executives – will be essential if the rule of law is to be restored to our markets. They must be both fair and seen to be fair if public and investor confidence and trust are to be restored.

Better Markets in the News:

Why Presidential Candidates are Talking about the Unique Threat Posed by Wall Street’s Megabanks: HuffPost by Dennis M. Kelleher 6/16/2016

Hank Greenberg Won Ruling on AIG Bailout, Will Appeal Anyway: Bloomberg by Sophia Pearson and Christie Smythe 6/16/2015

House Bill Nixes DOL Fiduiciary Rule’s Funding; Perez to Testify: ThinkAdvisor by Melanie Waddell 6/16/2015

What You Need to Know about Regional Bank Stress Tests: American Banker by John Heltman 6/16/2015

Hank Greenberg Wins Trial but No Damages over AIG Bailout: Bloomberg by Christie Smythe, Sophia Pearson, and Sonali Basai 6/15/2015

In AIG case, Surprise Ruling that Could End All Bailouts: The New York Times by Andrew Ross Sorkin 6/15/2015

Ex-AIG Chief Wins Bailout Suit, but Gets No Damages: The New York Times by Aaron M. Kessler 6/15/2015

News You Don’t Want to Miss:

Doing More, Not Less, to Save Retirees from Financial Ruin: The New York Times by Eduardo Porter 6/16/2015

Elizabeth Warren Dresses Down Jamie Dimon: Senator Fires Back at JPMorgan’s Manspainer-in-chief: Salon by Luke Brinker 6/12/2015