The Fox Telling Hens to Worry About Elephants: Goldman’s Cohn Warning about Clearing House Laughable When He’s Deregulating and Unconcerned about the Systemic Risks at Wall Street’s Too-Big-To-Fail Firms

The Fox Telling Hens to Worry About Elephants: Goldman’s Cohn Warning about Clearing House Laughable When He’s Deregulating and Unconcerned about the Systemic Risks at Wall Street’s Too-Big-To-Fail Firms

It is true that if a stampede of elephants came from far away and ran over a henhouse, that would be bad for the hens. But, the fox is the bigger, more immediate and lethal threat to the hens. After all, the fox is right outside the henhouse and is a recidivist hen attacker. That’s where the hens should focus their attention, energy and anxiety. Of course, that’s why the fox wants to distract the hens with other so-called threats like far-off elephants.

Today, Goldman Sachs and the other too-big-to-fail financial firms on Wall Street are the fox and American taxpayers are the hens. The Trump administration, with Goldman Sach’s former President Gary Cohn in the lead, is undertaking the most extensive deregulation of Wall Street in decades. That is going to make Wall Street’s biggest firms more dangerous, risky and fragile, particularly if capital cushions, derivatives regulations and enforcement are reduced substantially. No coincidence, that will also make them much more profitable, boosting their languishing trading operations hurt by the very regulations that are being weakened or gutted. However, that deregulation will inevitably lead to excesses, recklessness, illegality and, ultimately, another financial crash and taxpayers having to pay for more bailouts.

Rather than talking about any of that, Wall Street and its allies like National Economic Council Chairman Gary Cohn are trying to distract people by raising concerns about clearing houses (the elephant in the metaphor). First, central clearing of derivatives reduces systemic risk, not perfectly and not in all cases, but decidedly better than the pre-crash ad hoc arrangements and the other post-crash alternatives. Second, while clearing houses may pose some systemic risk, they do not currently and they just passed rigorous stress tests. Third, if they did pose an unacceptable risk, there are relatively easy ways to reduce it in terms of risk management, capital, margin and ownership structure, among other things. Fourth, everyone knew that clearing houses would likely be systemically significant when they were created, but they did not create new systemic risk. It was moving a type of systemic risk out of the too-big-to-fail firms to the clearing houses where the risks would be visible and properly regulated (rather than buried unseen and unregulated in the too-big-to-fail firms’ balance sheets).

Rather than talking about any of that, Wall Street and its allies like National Economic Council Chairman Gary Cohn are trying to distract people by raising concerns about clearing houses (the elephant in the metaphor). First, central clearing of derivatives reduces systemic risk, not perfectly and not in all cases, but decidedly better than the pre-crash ad hoc arrangements and the other post-crash alternatives. Second, while clearing houses may pose some systemic risk, they do not currently and they just passed rigorous stress tests. Third, if they did pose an unacceptable risk, there are relatively easy ways to reduce it in terms of risk management, capital, margin and ownership structure, among other things. Fourth, everyone knew that clearing houses would likely be systemically significant when they were created, but they did not create new systemic risk. It was moving a type of systemic risk out of the too-big-to-fail firms to the clearing houses where the risks would be visible and properly regulated (rather than buried unseen and unregulated in the too-big-to-fail firms’ balance sheets).

One has to wonder why, of all the significant systemic risks in the country, is Gary Cohn all of a sudden talking about clearing houses? He’d have some credibility if he talked comprehensively about systemic risks, including the much greater risks posed by Goldman Sachs and the other Wall Street firms, and if talked about the key role of capital, liquidity, counterparty exposure, derivatives regulation, and other critical remedial actions taken as a result of Dodd-Frank (which he did when he was at Goldman , but apparently has forgotten since he arrived at the White House). If he was genuinely concerned about systemic risks, he could have spoken out or maybe even stopped what appears to be the wholesale deregulation of the shadow banking system and the gutting of FSOC, which we spell out here.

Given he is a cheerleader for financial deregulation and attacks on the financial protection rules, it is clear Gary Cohn is not seriously concerned about real systemic risks, and instead this fox seems intent on first distracting and then plucking the hens.

The Challenge of Our Time: Deregulation Incentivizes One-Way Bets and is Sowing the Seeds of Another Catastrophic Financial Crash

The Challenge of Our Time: Deregulation Incentivizes One-Way Bets and is Sowing the Seeds of Another Catastrophic Financial Crash

The looming danger of the Trump administration’s all-out attack on financial regulation and how it will re-incentivize too-big-to-fail banks to make risky one-way bets that will likely lead to another financial crash is the topic of a paper written by Better Markets president and CEO Dennis Kelleher for a panel discussion he will be leading at the Institute for New Economic Thinking’s upcoming 2017 conference, “Reawakening: From the Origins of Economic Ideas to the Challenges of Our Time” coming up in Edinburgh, Scotland.

The paper, “Financial Reform Is Working, But Deregulation That Incentivizes One-Way Bets Is Sowing the Seeds of Another Catastrophic Financial Crash,” goes into depth on the recent de-designation of AIG as a systemically important financial institution and an examination of the claimed basis for deregulation, which is not only meritless, but also contradicted by the facts. He concludes by discussing insightful comments from former Fed Vice Chair Stanley Fischer and FDIC Vice Chair Thomas Hoenig that deregulating too-big-to-fail financial firms is incredibly dangerous and extremely short-sighted.

The Financial Stability Oversight Council (FSOC), a body comprised of federal and state financial regulators, is tasked with the unique mission to identify and respond to risks that threaten the financial stability of the U.S. Astonishingly, FSOC just recently voted to deregulate AIG, which not only failed spectacularly, requiring a $182 billion bailout, but also really ranks among the very worst financial institutions in terms of egregious and irresponsible behavior. As a result, it is no longer classified as a systemically significant financial firm and is no longer subject to enhanced supervision by the Fed. AIG, only nine years after being one of the main causes of the worst financial calamity this country has experienced since the Crash of 1929 and the Great Depression, now finds itself free of federal regulatory supervision.

The claimed basis for the Trump administration’s deregulatory efforts, that Dodd-Frank has been such a burden to banks that they would be less profitable and it would lead to lower lending and thus lower economic growth (as we write about here, here, and here ), is completely baseless. The banks and their allies have been predicting that the sky would fall and the world would come crashing down around them since the Great Depression in the 1930s. Instead, banks have prospered, as did the country, creating a strong, vibrant middle class, until the 2008 financial crisis destroyed so much that tens of millions of Americans had spent a lifetime building.

The claimed basis for the Trump administration’s deregulatory efforts, that Dodd-Frank has been such a burden to banks that they would be less profitable and it would lead to lower lending and thus lower economic growth (as we write about here, here, and here ), is completely baseless. The banks and their allies have been predicting that the sky would fall and the world would come crashing down around them since the Great Depression in the 1930s. Instead, banks have prospered, as did the country, creating a strong, vibrant middle class, until the 2008 financial crisis destroyed so much that tens of millions of Americans had spent a lifetime building.

The paper concluded with cautionary advice from two global financial statesmen on the dangers of deregulation and the need for good and smart people to stand up in the face of this deregulatory onslaught. Vice Chair of the Federal Reserve Board, Stanley Fischer had this to say on the deregulatory zeal taking over Washington:

“It took almost 80 years after 1930 to have another financial crash that could have been of that magnitude. And now, after 10 years, everybody wants to go back to the status quo before the great financial crisis. I find that really extremely dangerous and extremely short sighted. …[T]he pressure I fear is coming to ease up on the large banks strikes me as very, very dangerous.”

And a similar warning from FDIC Vice Chair Thomas Hoenig:

“In a country whose idol is prosperity, any attempt to tamper with conditions in which easy profits are made and people are happy, is strongly resented. It is a desperately unpopular undertaking to dare to sound a discordant note of warning in an atmosphere of cheer, even though one might be able to forecast with certainty that the ice, on which the mad dance was going, was bound to break. Even if one succeeded in driving the frolicking crowd ashore before the ice cracked, there would have been protests that the cover was strong enough and no disaster would have occurred if only the situation had been left alone.”

The INET conference offers an opportunity to discuss these and many other issues in greater detail. We’ll be reporting in greater detail on the event and the topics discussed as they happen and you can view the panel Better Markets is moderating on Monday, October 23, at 9:30 am Eastern by clicking here.

Bank Quarterly Results Prove…Again…Dodd-Frank is Working

Bank Quarterly Results Prove…Again…Dodd-Frank is Working

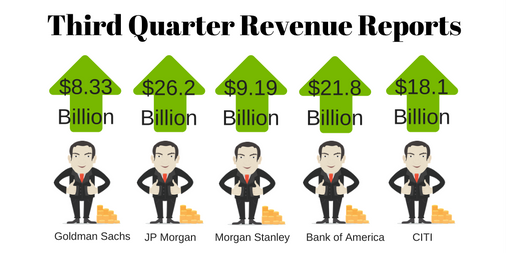

The song remains the same: the big banks reported their quarterly earnings over the past week and they all showed substantially the same results: increases in revenue, profits and lending, but a significant decrease in trading revenue. In other words, with more revenue coming from areas other than trading, the message is unmistakable: Dodd-Frank is working as intended as the banks rebalance their activities away from unproductive, usually socially useless trading and toward lending to the productive economy.

Results from Morgan Stanley, J.P. Morgan Chase, Goldman Sachs, and Citigroup all showed decreases in fixed income trading ranging from 8.2% at Morgan Stanley to 26% at Goldman Sachs.

Recall that in the years before the 2008 crash, lending to the real economy took a back seat to trading activities at the banks. These short-term, risky gambles were focused on delivering big bonuses to traders and executives, but these activities destabilized the banks, the financial system, and the economy.

That’s why rebalancing Wall Street’s biggest banks to focus on lending to businesses and hardworking Americans and away from big financial bets was a key objective of Dodd-Frank. While preventing financial crashes and bailouts grabs most of the attention of the law, that was also one of its key objectives.

This is an important message to keep in mind as the Treasury Department just recently issued the second of its reports on its plans to deregulate the financial system. Not only has Dodd-Frank been successful in eliminating or reducing the riskiest and most dangerous activities by Wall Street’s biggest financial firms, it has also succeeded in driving lending to the real economy. These results further prove that all the complaining that financial reform is hurting banks’ ability to lend, generate revenue or make a profit are still baseless and that the deregulatory zeal is meritless.

Don’t Ever Miss John Oliver’s “Last Week Tonight,” but if you did…

Don’t Ever Miss John Oliver’s “Last Week Tonight,” but if you did…

A segment on John Oliver’s most recent “Last Week Tonight” satirical program took a whack at the Equifax hack scandal and its ham-handed effort to force consumers into arbitration. If you have a few minutes to spare and need a laugh, check it out here.