Fact Sheet: The CLO Debate Is Just the Latest Wall Street Attack on the Volcker Rule

The first major hurdle to the recently finalized Volcker Rule was when a few community banks discovered that certain securities they own – TruPS CDOs – would be subject to the rule. Community banks brought this problem to the attention of the financial regulators, who acted quickly to understand the issues. But, the big Wall Street banks and their allies saw this as an opportunity to criticize the Volcker Rule and regulators more broadly. They exaggerated the small problem that affected only a handful of community banks and argued for what would have been a large loophole. The financial regulators sensibly rejected the baseless criticism and provided a narrow exemption for the particular securities.

Wall Street’s failed attempt to exaggerate and exploit the small, narrow TruPS problem won’t end their nonstop attacks on financial reform and the Volcker Rule. For example, they are trying to do the same thing with their latest campaign to get unwarranted relief for some of their own securities known as “collateralized debt obligations” or CLOs.

This is Wall Street’s typical attack plan: use any available issue, regardless of merit, in their unrelenting campaign to create after-the-fact loopholes in financial reform, including in particular into the Volcker Rule. Not surprisingly, the industry is trying to say the CLO problem is just like the recently solved TruPS issue. But CLOs are not TruPS, and JP Morgan Chase – the largest holder of CLOs – is not a community bank. Regulators and legislators must reject Wall Street’s baseless arguments and recognize that the CLO issue is largely a Too-Big-to-Fail bank issue.

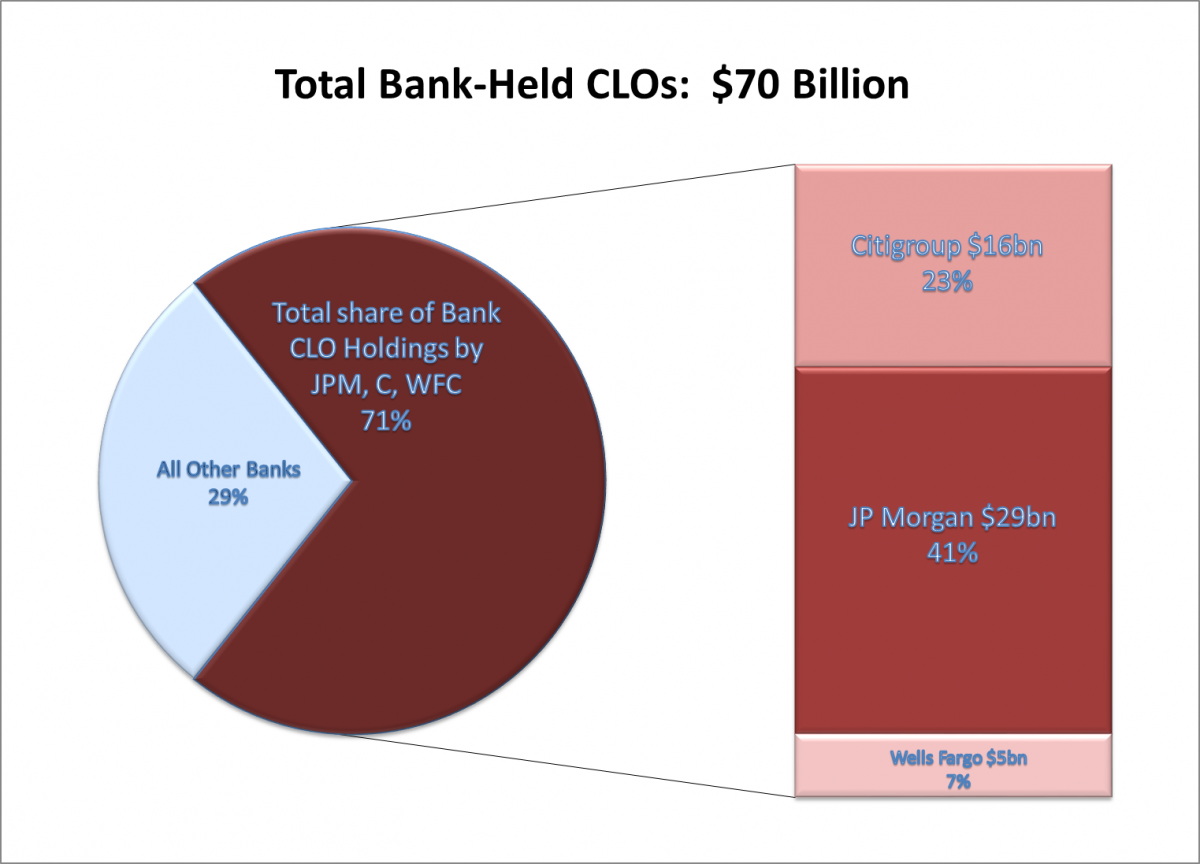

The biggest Wall Street banks were large holders of these products before, during, and after the financial crisis and today three of them account for 71% of all bank holdings of CLOs:

| Total Bank CLO holdings: | $70bn[i] |

| JPM CLO Holdings: | $29bn (41% of total bank CLO holdings)[ii] |

| Citigroup CLO Holdings: | $16bn (23%)[iii] |

| Wells Fargo CLO Holdings: | $5bn (7%)[iv] |

Background on Collateralized Loan Obligations

What are CLOs?

- CLOs are investment funds that consist of “leveraged loans”, (huge, low-rated, corporate loans) which can be swapped in and out by the manager throughout the life of the fund. Investing in a CLO is functionally identical to investing in a hedge fund that invests in this kind of loan.

- CLOs held by banks were – and continue to be – proprietary positions. Beneficial capital treatment of CLOs meant that banks could borrow cheaply and hold high-yielding CLOs on their books, capturing the difference as profit.

- The specific features of CLOs (when it will mature, the kinds of investments it can make, the rights and protections for each class of investor, etc.) are not publicly disclosed and are non-standardized, so it is impossible to know how many CLOs exist with any given feature.

- Importantly, it isn’t clear which CLOs, or how many, would be affected by any change in the rule.

The issues surrounding CLO treatment are NOT the same as those involved in the TruPS situation.

- CLOs are NOT backed by loans to small business or individuals. CLOs are backed by “leveraged loans”, or large junk-rated corporate loans typically used to fund corporate buyouts.

- CLOs are NOT owned broadly by community banks.

- CLOs have performed exceptionally well throughout the crisis and continue to be highly liquid and attractive securities.[v]

What does the Volcker Rule say about CLOs?

The Volcker Rule prohibits ownership of hedge funds, and CLOs are effectively hedge funds. But there are numerous ways that an existing CLO may become outside the scope of the Volcker Rule, so the rule’s impact on the vast majority of CLOs is likely zero.

- CLOs backed entirely by loans are excluded from the rule. Some CLOs are backed entirely by loans, others are backed by some mix of loans and other assets (bonds, derivatives, other securitizations). CLOs backed only by loans are explicitly excluded from the Volcker Rule and it does not prohibit banks from owning them in any way.

CLOs that are backed by a mix of loans and non-loans are generally covered by the Volcker Rule because they are identical to hedge funds – therefore banks have strict limits on how many they can own.

- Many CLO holdings are not considered “ownership interest” under the Volcker Rule. Even those CLOs that do not qualify for the loans exclusion may not be subject to the Volcker Rule if they don’t represent ‘ownership’ in the fund. The Volcker Rule considers “ownership” any position that has any feature of traditional securities ownership such as: the right to vote on the removal of the manager, or the participation in upside gains and downside risks of the investments. Traditional “debt” investments, like corporate bonds, do not contain any of these features and debt holdings are not considered “ownership” under the rule.

Certain CLOs may contractually provide investors with rights or protections that cause their investments to be considered “ownership interest” under the Volcker Rule. It is impossible to know how many CLOs have such features, since the documents are non-standard and not publicly available. CLOs without such features are not subject to the Volcker Rule.

- Many CLOs will mature before the Volcker Rule Divestment period is over, so banks will not have to sell them to comply with the rule. CLOs are generally structured as 10-year investments, and many existing CLOs will mature before July 21, 2019 (the maximum possible divestment date, including available extensions).

- Existing CLOs can potentially be restructured in order to be Volcker Rule compliant. Those CLOs that do not qualify for the exclusion, and are considered ‘ownership interest’ can still be brought into compliance with the rule if the stakeholders agree to amend the contract.

- New CLOs can be easily structured such that they do not fall under the Volcker Rule – and they are already being structured this way[vi]. Therefore, CLO issuance will not be affected in any way by the rule.

- Ultimately, very few CLOs may fall under the Volcker Rule’s ban on proprietary trading. Those CLOs that: are not already excluded from the rule, are considered ownership interests under the rule, will not expire before the divestment deadline, and cannot be restructured into compliance, must be sold. These are the only CLOs that banks will have to sell because of the Volcker Rule.

- The market for CLOs is very strong. The CLO market has been consistently liquid and outperformed most other securitizations throughout the crisis. Issuance rose 49% last year and demand remains strong.[vii]

- Banks would likely post profits on CLOs they need to sell in order to be compliant with the Volcker Rule. Because these securities are held on banks’ books at par value, due to accounting rules, they would likely realize significant gains if they were forced to sell these securities at current market prices.

[i] LTSA – Testimony of Elliot Ganz http://financialservices.house.gov/uploadedfiles/hhrg-113-ba00-wstate-eganz-20140115.pdf

[ii] JPMorgan Q3 2013 10-Q http://investor.shareholder.com/jpmorganchase/sec.cfm?doctype=Quarterly

[iii] Citi Q3 2013 10-Q http://www.citigroup.com/citi/investor/sec.htm