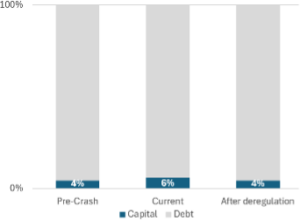

Let’s be clear about what is happening with capital at the largest U.S. banks: those banks and their army of lobbyists – and allies in the Trump administration and at the banking regulatory agencies – are working overtime to get capital as low as possible. In fact, their goal – which they are likely to achieve and which their leading trade group, the Bank Policy Institute (“BPI”), has publicly outlined – is to get capital as low as it was before the horrific 2008 Financial Crisis (“2008 Crash”). That was when those gigantic banks had so little capital (about 4% capital/96% debt) that they collapsed and had to be bailed out by taxpayers while 27 million Americans were thrown out of work and millions were thrown out of their homes due to foreclosures. That’s what’s at stake when talking about bank capital.

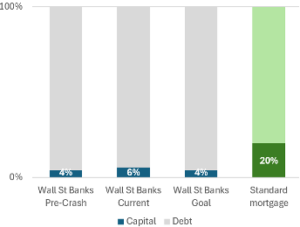

Figure 1: Large bank capital v debt funding compared to a standard mortgage

Source: FR Y-9C as of December 2024 and 2007, Financial Crisis Inquiry Report, and authors’ calculations

Once the industry’s agenda to substantially weaken each part of the capital framework is pushed through (detailed below), it will all add up to a reckless reduction of capital for the largest banks down to the pre-2008 Crash level of 4% – that’s 400% lower than the capital cushion banks require a Main Street homeowner to have for a mortgage down payment. A 4% capital level means if a giant Wall Street bank lost just 4% then it would be bankrupt, which is grossly inadequate given the many complex, dangerous, and high risk activities these banks engage in. This isn’t a theoretical risk; 4% losses can happen relatively easily if not frequently. For example, those banks wouldn’t even be able to absorb losses on 10-year U.S. Treasury securities, which had a 5% loss in value within a week this past April during the market turmoil.

The fight over banks having enough capital to absorb their own losses and avoid bankruptcy and bailouts can seem complex, but it’s really pretty simple: the lower the amount of capital a bank has, the higher the bonuses for the CEO and executives. That’s because lower capital means a higher return on equity (“ROE”), and the higher the ROE, the bigger the bonuses – hundreds of billions of dollars. The key fact to remember is that ROE goes up – bonuses go up – when bank capital goes down.

But that’s not the only reason. The ugly truth is that those gigantic banks don’t want to have enough capital because they are thought to be “too big to fail,” a status they want to maintain because it means that the government will bail them out rather than let them fail and, they claim, cause another Great Depression. Ultimately, they want to have the taxpayer cover the losses when they fail from not having enough capital. Think about it from the bank’s perspective: would you rather have enough capital to prevent failure and lower compensation or too little capital with billions in extra compensation and the government to bail you out when you fail? Thus, while always denying it, Wall Street’s biggest banks want to be too big to fail, a key unstated reason for wanting to have as little capital as possible.

The critical questions to remember are (1) who will provide the capital to prevent bank failure and (2) when? It’s either the bank before it fails or taxpayers after it fails to prevent the bank’s bankruptcy. That’s what a taxpayer bailout is: it’s nothing more than a capital injection after the fact because the bank didn’t have enough of its own capital before it failed. Banks having too little capital so they can have higher pay is nothing but shifting the risk of capital losses from the bank to the taxpayer. Again, that’s why it’s critical for banks to have enough loss absorbing capital to prevent their failure and to prevent taxpayers from having to inject capital into a bank afterwards to prevent its failure.

Meanwhile, these banks mislead the public if not make outright false statements about their capital and ability to absorb losses in crises. For example, JP Morgan Chase touts a capital ratio of over 15%, making it seem as if they can take 15% of losses before going bankrupt. But this is a “risk adjusted” capital ratio (detailed below) that does not represent their actual loss taking capacity. The amount of capital a bank has that is not risk adjusted – the 4% discussed above – is what matters, and lowering that is the ultimate goal of Wall Street’s biggest banks.

The industry’s push for lower capital is a multi-step, multi-year plan that hides the ultimate goal by weakening each component of the capital framework separately. This fact sheet details those deregulatory steps, which add up to substantially reduced capital across the largest banks:

- A reduction of capital cushion from 6% to 4%, the same grossly inadequate capital level these banks had in the years before the 2008 Crash.

- A payout to shareholders of over $200 billion, which is capital the banks should instead retain to have enough to absorb losses.

- An increase in leverage to 23:1 from 17:1.

Why is capital important and what is the capital requirement framework?

Banks engage in many complex and high-risk activities, many of which result in profits, but some of which result in losses. Some of those losses are foreseeable and predictable, but some, especially potentially the biggest losses from, for example, crashes like 2008, are not.

Capital is meant to absorb the expected and unexpected losses from the bank’s profit-making activities. If a bank doesn’t have enough capital to absorb its own losses, then it goes bankrupt. However, as noted above, if a bank is so large, complex, interconnected and important – like the largest banks on Wall Street – then its failure could disrupt the financial system and the economy and cause crashes and crises. To prevent that damage, governments bail out those banks by giving them the capital they should have had to prevent bankruptcy. That’s why those banks are referred to as “too big to fail.”

Put differently, either those gigantic banks have enough capital to prevent their failure in the first place or the government – meaning taxpayers – provide the banks with capital to prevent their failure once their losses exceed their capital levels. That’s why it is so important for banks to have adequate capital – to prevent their failure and eliminate the need for taxpayer bailouts.

We already have seen the consequences of capital levels that are too low with the 2008 Crash. Unfortunately, the lesson was not learned, and capital was substantially weakened for many banks starting in 2018, resulting in the collapse of Silicon Valley Bank and others in 2023 which directly cost Americans more than $40 billion in bailouts, but really cost much more due to insuring uninsured deposits, contagion, credit contraction, and as much as 1% lost GDP.

To avoid another crash like the 2008 Crash and make sure that the largest banks had enough capital, the regulatory agencies after that crash put in place a capital requirement framework for the largest banks that required them to increase their capital levels. This decreased their likelihood of failure and the need for taxpayer capital injections to prevent their failure (which is what a bailout is). Generally, the framework is based on two separate but complementary requirements:

- A risk-based requirement that sets capital requirements for specific activities based on their estimated riskiness. So, the riskier an activity is believed to be, the more capital a bank should have for that activity to serve as a loss buffer. Aggregating requirements across activities sets the total capital requirement.

- A leverage-based requirement that is applied across all activities, ensuring banks have a minimum capital cushion to absorb losses regardless of the risk any particular activity is believed to pose and capturing instances in which the risk-based requirements are missing or underestimating risks.

Put simply, risk-based requirements define the capital cushion to protect against a loss percentage for specific assets, whereas the leverage requirement defines the capital cushion to protect against a loss percentage across all assets. Therefore, risk-based requirements vary from bank to bank based on the perceived riskiness of their activities, whereas the leverage requirement is the same for the largest banks – currently 5 percent across all financial activities.

The ultimate goal of the largest banks for the capital requirement framework

The largest banks want to weaken the capital framework significantly to boost profits, ROE, and bonuses. To achieve this, the banks have to get both the risk-based and leverage-based requirements lowered, and they and their lobbyists are working very hard towards this.

Ultimately, they want to increase their leverage greatly while still having the risk-based requirement as the “binding” requirement, or – put another way – the requirement they use to manage their business. In this way, they can maximize their overall return on equity as well as the return on equity of specific activities/ lines of business, a standard practice for the largest banks.[1]

The industry’s deregulatory strategy and ultimate impact on capital

Each of the framework’s components is being attacked separately by the industry, a strategy they are using so that the public does not see their ultimate endgame. That is, by attacking each component on its own, it is easy to miss what the total impact will be to the capital framework once all the pieces are put together.

The first step is already underway – lowering the leverage requirement. This summer the federal banking agencies put out a proposal that could have been written by Wall Street’s biggest banks because it will substantially reduce their leverage requirement.

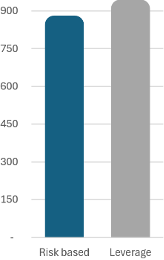

Currently, the risk-based and leverage capital levels of the largest banks are close.[2] After the proposal on the leverage requirements is finalized as the new requirement – which is virtually certain given a majority of the banking regulators have already signaled their clear intent to enact it as proposed – required leverage capital will decrease significantly, just as Wall Street’s banks want.

| Figure 2: Current capital dollars for each requirement

Source: FR Y-9C as of December 2024 |

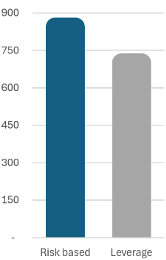

Figure 3: Current capital dollars for risk-based requirement and estimated for leverage requirement

Source: FR Y-9C as of December 2024 and authors’ calculations |

Once Wall Street’s banks get the leverage requirement decreased, they and their allies at the bank regulators will turn their attention to reducing the risk-based requirement, which has three components:

- A baseline requirement,

- A buffer that accounts for the systemic importance of the largest banks (the global systemically important bank surcharge, or “GSIB surcharge”), and

- A buffer associated with the stress test (the stress capital buffer, or “SCB”).

The industry is seeking to weaken each component, as they have written about many times (see links immediately below where BPI has made the intent clear). The goals are to:

- Water down the so-called Basel Endgame proposal so that it reduces baseline capital (rather than increase capital as was originally proposed in 2023).

- Lower the GSIB surcharge by updating key parameters.

- Weaken the stress test even further than already has been done so that most of the largest banks are floored at the minimum buffer amount.

Taken together, capital would be substantially reduced from around 6% to 4%, the same capital the largest banks had leading up to the 2008 Crash. This would be a reduction in capital of over $200 billion.

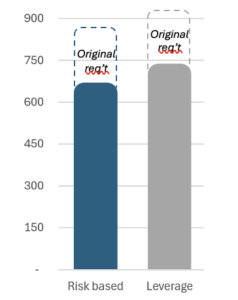

| Figure 4: Estimated capital dollars for each requirement

Source: FR Y-9C as of Dec. 2024 and authors’ calculations |

Figure 5: Percentages of capital and debt funding of large bank financial activities

Source: FR Y-9C as of December 2024 and 2007, Financial Crisis Inquiry Report, and authors’ calculations |

Conclusion

The only thing standing between a failing Wall Street megabank and a taxpayer bailout is the amount of capital a bank has to absorb its own losses. The less capital a bank has the higher the likelihood it will fail and get capital injections from the government to prevent its failure – bailouts paid for by taxpayers like happened in the 2008 Crash and again in 2023. Over the years the largest banks and their lobbyists have pushed a misleading – and at times false – narrative on the American public about bank capital so they can get their agenda of lower capital enacted.

Now the industry, its lobbyists, and its allies – including those at the banking regulators who know better and who are supposed to prioritize the public interests not Wall Street’s special interests – are seeking to bring capital back down to the reckless levels that were in place in the years before the 2008 Crash to maximize return on equity, executive bonuses, and payouts to shareholders. Once each piece of Wall Street’s deregulatory agenda is completed, Wall Street’s megabanks will once again fill their pockets with the profits brought in by lower capital while putting Main Street families on the hook to pay for the bailouts to cover the losses that result from the banks having too little capital in the first place. Capital levels must be high enough now – before losses and crashes – so that the American people don’t have to pay for them after those losses and crashes happen.

Appendix

Major misleading and false claims made by the industry around bank capital requirements

The largest banks and their lobby consistently make many misleading and false claims about bank capital requirements. The biggest are:

- They have high capital ratios, which means they are well-positioned to withstand losses from economic or market stress.

- While it is true that the risk-based capital ratios for many of the largest banks are comfortably above their minimum requirements (e.g., JP Morgan having a risk-based ratio of 15.1% vs its requirement of 11.5%), risk-based ratios are not a true reflection of loss absorption capacity.

- Risk-based ratios adjust the value of assets and other activities for the riskiness of financial activities. Those adjustments are estimated and can underestimate the size of risk. For example, US Treasury securities are assigned zero risk even though their values can be volatile as in March 2020 and April of this year.

- Banks also can optimize the risk-adjusted value of their financial activities based on the rules. For example, the largest banks are seeking to classify many types of lending as securitization activities, which receive only a 20% risk weight (as opposed to e.g., a corporate loan which has a 100% risk weight).

- A true reflection of loss absorption capacity is the leverage capital ratio, which simply represents the percentage of losses a bank can absorb across all its financial activities without any of the estimated risk adjusting. This ratio shows a much lower loss absorption capacity of 6% across the largest banks.

- They consistently pass the stress test, which proves they have sufficient capital to withstand a major economic and financial crisis.

- As Better Markets has detailed many times before (here, here, and here), the stress test has been woefully un-stressful for years, even before it was significantly weakened in 2018.

- The most material changes in 2018 were the removal of two key assumptions: a growing balance sheet (which has been the case historically under stress) and banks continuing to pay dividends throughout the stress period. Removal of these assumptions has had a huge impact on stress test results (see estimates here).

- On top of those deficiencies, the stress test always has failed to account for key risks, especially correlation and knock-on effects and risks to funding.

- Their resiliency during the pandemic proves that they are strong enough to withstand severe stress.

- Claims that the 2020 pandemic somehow proved banks were sufficiently capitalized and thus a “source of strength” are wrong. While higher capital requirements for the largest banks did make them more resilient entering that crisis than they otherwise would have been, these requirements simply bought time for the Fed to roll out massive programs providing trillions of dollars of financial market support as well as regulatory relief. This propped up the value of financial assets, boosted banks’ trading revenues, and freed up capital to return to shareholders.

- In reality, the large banks only had to be a “source of strength” for about two weeks after the onset of market stress in early March 2020. The Fed began providing unlimited support to the financial system in mid-March.

Methodology for estimates of capital reduction and leverage increase

The historical leverage of the largest banks in 2007 was obtained from the Financial Crisis Inquiry Commission Report, page 65. Leverage figures excluding off-balance sheet activities were used. Each bank’s leverage from that report was weighted by its total assets in 2007 to compute aggregate leverage.

All estimates for future capital reduction and leverage increase are based on data reported through the FR Y-9C for the eight U.S. global systemically important banks (“GSIBs”) as-of December 31, 2024. The aggregate figures shown in this fact sheet are weighted aggregate figures.

The estimates for the reductions of the enhanced supplementary leverage ratio requirements for each bank were based on the federal banking agencies’ proposal from June of this year (90 FR 30780; July 10, 2025).

For analysis of the risk-based requirement reductions, assumptions are based on articles published by the Bank Policy Institute (“BPI”). Our assumptions are:

- Basel Endgame finalization leads to an RWA reduction of 10%. BPI has stated that from their perspective keeping modifications to the baseline capital requirement “capital neutral” means neutral to 2019 ratios when Federal Reserve Chair Powell stated that capital in the system is “about right”. At that time capital ratios were 18% lower. We use 10% to be conservative.

- GSIB surcharge changes are made so that “method 2” GSIB surcharge requirements equal the values estimated in a note put out by BPI.

- The stress capital buffer (“SCB”) is weakened further so that six of the eight GSIBs are floored at the 2.5% minimum. This year, five of the eight GSIBs were assigned the floored requirement, with one GSIB yet to be assigned. For the analysis, the floor is not assumed for Goldman Sachs and Morgan Stanley because of the size of their trading operations would make it very difficult to reach the floor. For those banks an SCB of 3% is assumed for Goldman Sachs (3.5% SCB requirement this year) and 3.5% for Morgan Stanley (yet to be published for this year).

[1] For example, see the business line-specific return on equity from the latest annual report of JP Morgan Chase.

[2] Note that leverage capital level is slightly higher because it is a broader definition of capital – tier 1 capital – than the common equity tier 1 used for risk-based.