Service members, veterans, and their families are disproportionately targeted by financial scams and financial predators. That’s painfully obvious whenever one walks outside the gates of a military base: paycheck lenders, check cashing companies, loan companies, used car salesman, and many more businesses with questionable practices surround the streets next door to where service members live and work. Less obvious are other financial traps, including those that lurk online or come from more mainstream financial firms, from credit and debit card tricks to loans of all types.

That’s why Congress has passed, and law enforcement has traditionally ensured, that our service members and veterans are protected in the financial marketplace. These populations and their families make many sacrifices to protect their country; they shouldn’t be left to fend for themselves from financial scammers, predators, and criminals. But that’s exactly what the Trump administration is doing by shutting down the Consumer Financial Protection Bureau (CFPB or Bureau) as well as refusing to enforce financial protection laws more broadly.

Introduction

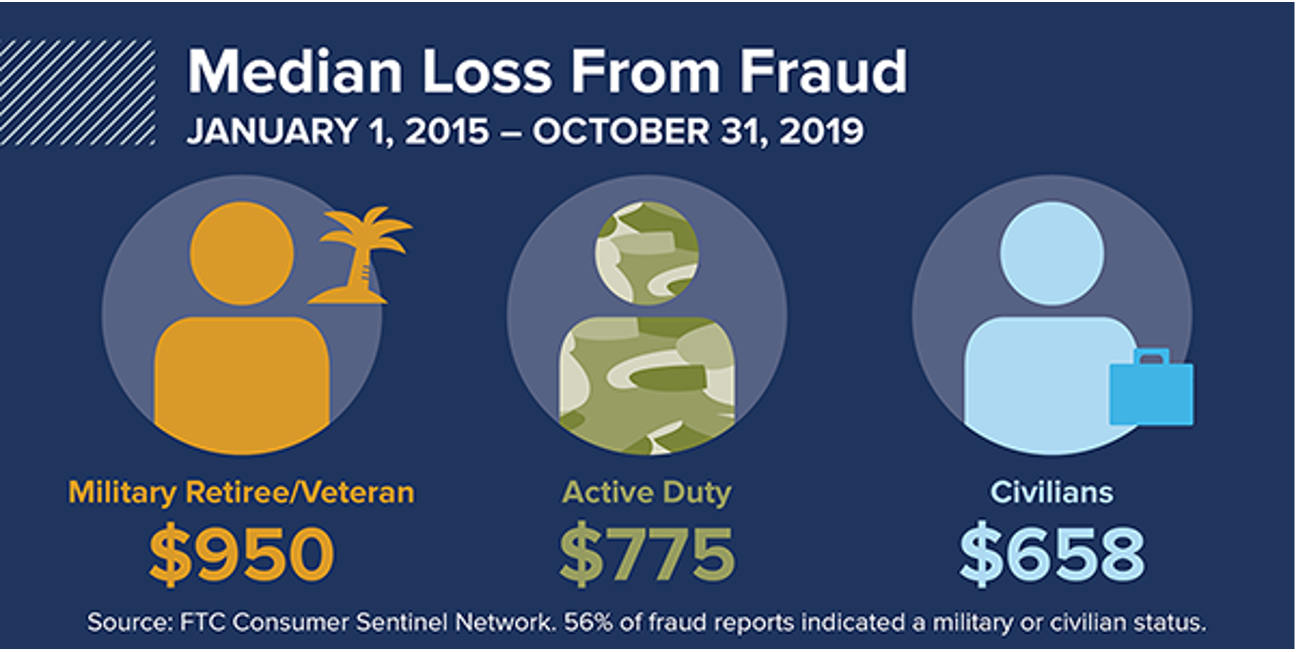

Service members, veterans, and their families are being ripped off frequently and in significant amounts: they lost a total of $584 million to fraud in 2024, a nearly 25% increase over 2023. According to one survey, veterans are twice as likely to be the target of a scam, with 16% of veterans saying that they have lost money to fraud and 78% say they were specifically targeted because of their military service.

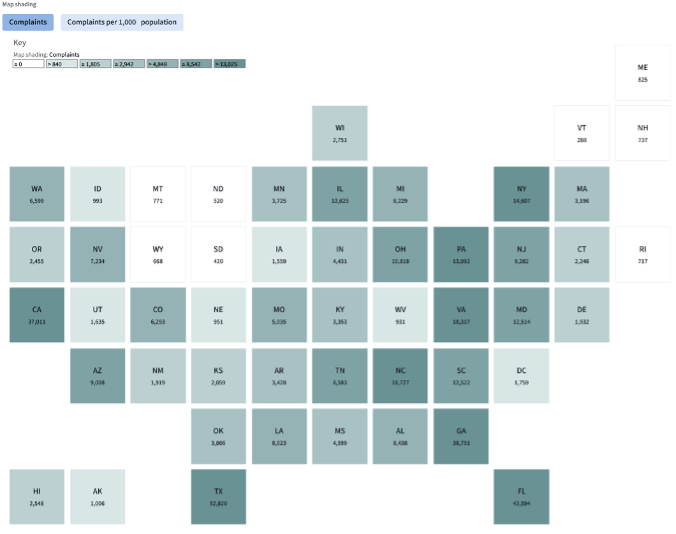

The shockingly high level of financial harm to veterans and service members is confirmed by complaint data submitted to federal consumer protection agencies. For example, in 2024, military-related complaints filed with the Federal Trade Commission (FTC) relating to credit bureaus, banks and lenders, and debt collectors rose by 20% from 2023. Since the CFPB was created in 2011, it has received more than 400,000 complaints from service members and has been responsible for recovering approximately $363 million in restitution for military-connected families. These complaints and following restitution effect servicemembers, veterans, and their families in every state across the country as the below map shows.

Source: CFPB Consumer Complaint Database

Financial scams are so prevalent in the military community that the Department of Veterans Affairs (VA), FTC, CFPB, and other federal agencies all have dedicated websites and even created an interagency task force, called VSAFE, to inform the military community of the financial threats that they face from scammers, fraudsters, and predatory financial institutions.

Laws Related to Service Member Protection: Supervision and Enforcement Imperiled

Recognizing the unique financial vulnerabilities of service members, veterans and their families, Congress has passed several laws to give greater consumer protection to these populations, such as the Servicemembers Civil Relief Act (SCRA) and the Military Lending Act (MLA).

The SCRA, originally passed in 1940, is still incredibly important to protect service members from a wide variety of civil misconduct, including protecting them from foreclosures and illegal repossessions. The Department of Justice (DOJ) is largely responsible for protecting service members that have had their rights violated under SCRA provisions. During the 2008 financial crisis, many service members had their homes illegally foreclosed on, eventually leading to a $25 billion settlement with the largest mortgage providers in the country. In addition to mortgages, the SCRA also allows service members to terminate a lease due to their military service. In one example, the DOJ was able to return almost $100,000 to service members that were illegally barred from terminating their car leases. Since 2011, the DOJ has returned $481 million to over 147,000 service members through SCRA enforcement. This important consumer protection law allows service members to focus on their mission in defending the country. Continued enforcement of the SCRA is under threat, with a DOJ increasingly focused on immigration enforcement and turning away from white collar crime investigations.

The MLA caps the interest that can be charged to service members, bans mandatory arbitration, limits the number of fees that can be assessed, as well as provides a number of other important protections. After the creation of the CFPB, that agency became responsible for ensuring that financial institutions were complying with the MLA and issuing enforcement actions on any financial institution that was not in MLA compliance. In 2018, under the first Trump Administration, the CFPB stopped supervision of the MLA, which triggered many veterans and military service organizations to push back against the new policy, even publishing ads to raise awareness of the issue. President Trump’s latest Acting Director of the CFPB, Russell Vought, stopped MLA supervision again in 2025.

With the second Trump Administration attempting to shut down the CPFB entirely, and the recent passage of the misnamed One Big Beautiful Bill which cuts the CFPB’s funding by almost half, it is unclear how — if at all — the supervision and enforcement of the MLA will be conducted going forward. Acting CFPB Director Russ Vought has announced plans to shut down the agency “in the next two or three months.” To date, no one in the Administration has articulated plans for how the MLA will be supervised and enforced after the plan of shutting down of the agency goes forward.

Congress, knowing how vulnerable military families were to lapses in consumer protection, created the Office of Servicemember Affairs within the CFPB when it passed the Dodd-Frank Act in 2010. That Office is focused exclusively on service members, veterans, and their families. It has provided resources, advice, and a single point of entry that makes it easy for these populations and their families to get their issues addressed expeditiously. That, of course, is particularly important for service members who are often being transferred, deployed, or otherwise moved around as part of their duties. The status of those working in OSA remains in flux as Trump continues his efforts to shutter the agency.

Currently, the Trump Administration is continuing at least some of the lawsuits regarding MLA violations started under the Biden Administration. One of those cases has already been settled out of court. FirstCash Inc. and its subsidiaries operated retail pawn shops and charged servicemembers more than the 36% interest rate allowed under the MLA. In the settlement. FirstCash agreed to pay $5 million to harmed servicemembers and $4 million to the CFPB’s victim’s relief fund. It is unclear how or whether this relief fund will be deployed if the Administration shutters the Bureau, as promised.

However, the MLA and the SCRA are not the only way that the CFPB and other agencies protect service members and their families. They also protect military-connected families by enforcing generally-applicable consumer protection laws, which have also been massively scaled back under the new administration.

Although the CFPB’s new leadership claims that it prioritizes service members as part of its new reduced enforcement priorities, some of the Bureau’s recent actions contradict that claim. For example, the CFPB withdrew its $95 million case against Navy Federal Credit Union (NFCU), the largest credit union in the country, which also has a large military customer base, for illegally issuing surprise overdraft fees against service members and their families. As a result, the credit union gets to keep the $80 million it was supposed to refund to its ripped off customers. It has been reported that NFCU also denied more than 50% of Black mortgage applicants, which is 100% higher than the denial rate for white mortgage applicants. That also disproportionately affects service members and their families, given that they make up the membership base of the credit union.

Rewriting the Rules to Leave Service Members Behind

Moreover, the CFPB is rewriting rules related to non-bank “larger participants” in financial markets. Entities with this designation are subject to CFPB oversight, with supervisors charged with examining the institutions for compliance with relevant consumer protection laws. The Bureau recently put forward a proposal to exempt a wide swath of now-covered auto lenders from larger participant status. If finalized, nearly all auto lenders serving subprime customers would be immune from Bureau supervision. Coincidentally, these lenders are more likely to serve service member customers and have higher rates of loan default and repossession. And in the past, the CFPB has recovered nearly $75 million in restitution and penalties from these lenders, affecting 1.36 million customers, including more than 50,000 service members.

The CFPB has likewise released a proposal to exempt debt collectors from larger participant status, again allowing these firms to escape routine oversight. Past data collected by the Bureau demonstrates that servicemembers and veterans are more likely to file complaints about debt collectors than civilians. The same study found that two out of every five complaints filed by servicemembers with the CFPB are about debt collection. Further, confusion about the application of VA medical benefits can increase the rate of surprise medical debt for servicemember and veteran populations, resulting in incorrect debt collection attempts. Given that servicemembers and veterans are more likely to have frequent and complex interactions with consumer debt collectors, and the consequences of having debt are greater for these populations, compliance with relevant consumer financial laws is also of heightened importance. As a CFPB report from earlier this year documents, “debt may affect whether servicemembers receive and maintain a national security clearance.” The report adds that “in addition to possible loss of their security clearance, servicemembers who fail to pay their debts also face other unique consequences such as military disciplinary action, delayed career progression, and termination from employment.” Research also found that a significant number of servicemember complaints about debt collection involved collectors who contacted or threatened to contact a servicemember’s commanding officer — which could jeopardize the servicemember’s security clearance. In other words, being hounded by consumer debt collectors out of compliance with relevant law affects the welfare of individual servicemembers and may also impact our nation’s overall military readiness.

Finally, much of the guidance that new CFPB leadership has now withdrawn provided benefits to service members and their families. For example, the CFPB previously outlined its authority and procedures for conducting supervisory examinations of financial institutions regarding financially risky practices impacting active-duty service members and their dependents. But despite the Bureau’s stated commitment to service members, this guidance was inexplicably withdrawn in May 2025 along with dozens of other rules and guidance documents. These actions make it clear that the administration is not going to enforce the laws to protect service members, veterans and their families.

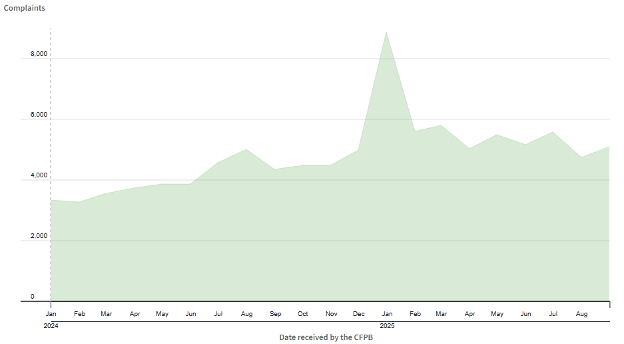

This comes at a particularly harmful time, as CFPB data shows that complaints from service members and their families spiked at the beginning of the year, shortly before the Trump Administration started its assault on the Bureau and attempted to shutter it entirely.

Source: CFPB Consumer Complaint Database

With all of the uncertainty surrounding the CFPB and the OSA, it is also unclear if they will continue to produce annual reports which highlight trends found in the complaint database focused on the military community. These reports are used to find new and emerging threats to servicemembers and their families financial health. They not only allow give other federal agencies crucial information to fight these threats but also empower veteran and military service organizations to better inform their communities about the dangers of predatory financial institutions. The most recent annual report was released in September 2024 and covers the previous year. The 2025 report release date has not been announced.

Crypto Scams: An Escalating Harm

Additionally, as crypto is more aggressively marketed and intertwined with traditional finance, it has skyrocketed in its use in fraud and scams, including those focused on service members and veterans. Several official government websites warn veterans, service members, and their families that crypto is a common way that scammers try to get payments from their victims. The Better Business Bureau Institute found that cryptocurrency/investment scams were the riskiest type of fraud facing veterans, with median losses of $5,000 for those affected – nearly 40 times higher than the median amount lost to other types of scams. The military has likewise warned service members that online scammers may attempt “romance scams” – luring service members to believe that a fraudster is in love with them – or impersonation crimes, where fraudsters steal service members identities to make heartfelt pleas for donations. In either case, perpetrators typically demand to be paid in Bitcoin.

This harm is being ignored by the current administration as it blindly pushes crypto friendly policies that will inevitably continue to harm the military community. While currently the places that the military community goes for information on scams mention crypto, that is not sufficient and is almost certain to be deleted soon and replaced with pro-crypto marketing materials. Reporting on crypto-related scams, such as the FBI’s Internet Crime Report, could also come to a halt, making it harder to highlight how dangerous crypto is to the military community.

Conclusion

With the Trump Administration’s all-out assault on consumer protections, service members, veterans, and their families will lose Congressionally mandated protections. These communities remain particularly vulnerable to financial scammers, and the rise of crypto and internet-related crimes only make these issues more important. Financial readiness in the military is a national security issue, as servicemembers need to be able to focus on their important jobs of protecting the nation, as international threats continue to rise. When they are worried about being ripped off by a financial company that they should be able to trust, that directly leads to harm in force readiness. For example, servicemembers that are victims of fraud and abuse in the financial industry can lose access to their security clearance, through no fault of their own. This leaves dangerous gaps in our military readiness while the issues are resolved. By shuttering the CFPB and attacking consumer protection laws within the SEC, banking agencies, and the DOJ, the Trump Administration has turned their backs on the financial well-being of servicemembers, veterans, and their families when they need them the most.