Introduction

At the beginning of the year, we questioned whether a Trump administration filled with wealthy individuals and Wall Street executives could fulfill its promises to America’s working class. The nomination of Paul Atkins, a champion of deregulation, to be chair of the Securities and Exchange Commission (SEC) did not bode well for an agenda favorable to ordinary retail investors. As Dustin Guastella wrote in The Guardian one year ago, “loose regulatory oversight” would “ensure that whatever growth the Trump economy generates, the gains will accrue mainly at the top.”

One year later, to say that regulators at the SEC and elsewhere have pursued “loose regulatory oversight” would be an understatement. The SEC is in the process of demolishing investor protection. Once known as the investor’s advocate, it is now the financial industry’s advocate.

For this reason, it should not be surprising that those “at the top” are way more optimistic about the economy than the rest of America. Politico reports: “Never mind the crummy vibes emanating from consumer surveys or public polling on the state of Trump’s economy. Nearly a year into the president’s second term, the CEOs of big banks and asset management shops that run Wall Street feel bullish.” That’s probably because the SEC and other regulators are prioritizing their interests rather than the interests of hardworking Americans who are struggling to make ends meet.

Vice President JD Vance said at the Republican National Convention in 2024 that his party was done “catering to Wall Street” and would instead “commit to the working man.” The extent to which the SEC has done the opposite is astounding. Workers are often the retail investors who view the stock market as a way to save for a house, pay for college, or enjoy their retirement. The SEC used to protect these retail investors—the shareholders of public companies. Now, the SEC should be known as something else—the Shareholder Exploitation Commission.

Public Markets

The SEC has spent the last year making it harder for shareholders—the ultimate owners of a public company—to have a say in how the companies they own should be run. It has done this by:

- Making it easier for companies to obtain a letter from the SEC saying it will not object if a company chooses to exclude a shareholder proposal from its proxy materials

- Rescinding guidance that made it harder for companies to exclude shareholder proposals

- Issuing guidance making it more difficult for investors to engage with companies on critical issues like executive compensation without triggering restrictive disclosure requirements

These actions favor corporate management rather than ordinary investors, such as the small group of nuns in Kansas who only want to advocate for change in the companies in which they invest.

The SEC is also trying to limit the information shareholders receive about the companies they own. Chair Atkins’s plan to “Make IPOs Great Again” centers on reducing the disclosures that public companies must provide to investors. The problem is that disclosure is precisely what protects ordinary investors from the predations of Wall Street and corporate executives. For example, Chair Atkins held a roundtable on executive compensation disclosures that focused on reducing those disclosures and has said the SEC needs a “re-set” of the rules that require disclosures about executive compensation. Yet executive compensation disclosures reveal the following facts:

- CEO pay has risen by 1,085% since 1978 compared to 24% for typical workers’ pay

- CEOs now make 290 times as much as the typical worker

- CEOs now make over nine times as much as even the top 0.1% of workers in the economy.

Chair Atkins has not said how the SEC letting CEOs hide how much more money they make than ordinary workers would help regular people rather than corporate elites.

The SEC further issued guidance saying that companies may force shareholders into mandatory arbitration. Corporations have long championed mandatory arbitration provisions. That’s because mandatory arbitration almost always favors corporations and rarely results in a win for investors. Perhaps most importantly, mandatory arbitration prevents shareholders from suing in court. As a result, mandatory arbitration is nothing more than a way to stifle investor complaints.

Private Markets

At the same time the SEC is making it harder to be a shareholder of a public company, it is trying to steer ordinary retail investors into private market assets. This favors the private market firms that are looking for an expanded investor base since money from the institutional investors who typically invest in the private markets is drying up. Private market assets are more opaque, more illiquid, and more expensive than publicly traded stocks and bonds, but that hasn’t stopped the SEC from taking the following actions to try to induce retail investors to enter the private markets:

- Touting the supposed benefits of private market assets for retail investors.

- Permitting an exchange-traded fund that intends to invest in private credit to start trading despite concerns raised by the staff about the liquidity and valuation of such assets.

- Allowing individuals to self-certify that they qualify as the “accredited investors” to whom private market assets may be sold, even though these individuals may not have the resources to conduct proper due diligence or to absorb the losses that may occur.

The risk of investing in the private markets is why the SEC has historically limited private fund sales to institutional investors and high net worth individuals who can “fend for themselves,” and one recent high-profile example shows why. David Gentile, the former private equity executive who a few weeks ago had his seven-year prison sentence for fraud commuted, preyed on ordinary people who technically qualified as accredited investors. Gentile perpetrated a $1.8 billion securities fraud scheme that ensnared 17,000 investors across the United States, all of whom met the definition of an accredited investor eligible to participate in private market securities transactions. Gentile’s victims show the perils of an overly broad definition of an accredited investor, and of allowing ordinary retail investors to invest in the private markets. His victims included:

- Catherine Kominos, 66, a retired engineer in Virginia who invested $50,000. “I’m a senior citizen,” Kominos said. “I need that money. It’s not like I’m a jet setter or a wealthy person.”

- Lou DeLuca, 76, a retired schoolteacher from Brooklyn who invested $100,000.

- Jeff Lipman, 72, a retired dentist living in Boca Raton, Florida, who lost $300,000.

Given that even large institutional investors lose billions of dollars in the private markets, the SEC’s push to eliminate the longstanding restrictions on sales of private market assets to ordinary retail investors does not exemplify a commitment to American workers, but rather to the interests of Wall Street. Perhaps most tellingly, surveys consistently show that ordinary investors do not want more options to invest in the private markets. The Wall Street Journal found that only 10% of investors are dissatisfied with their current 401(k) plan offerings and want more nontraditional options like private equity and private credit. Research conducted by AARP similarly found that:

- Most adults do not think it’s important to have the ability to invest in private market investments (61%) or cryptocurrency (73%) in their workplace retirement savings accounts.

- Interest in private market investments declines sharply when people learn about their fees, liquidity, transparency, and risk. Similarly, additional information about cryptocurrency investments reduces the already low interest by roughly 10 percentage points.

- Most Americans are uncomfortable with being automatically enrolled in funds in their workplace retirement savings accounts that include private market investments (68%) or cryptocurrency (75%). This resistance is particularly strong among older adults.

So the SEC’s push to allow private market sales to ordinary retail investors willfully ignores the needs and preferences of working Americans and instead allows the Wall Street firms who stand to profit from such investments to achieve what they have long viewed as their holy grail.

Crypto

As troubling as the alignment between the SEC and the private funds industry is at the potential expense of retail investors, the risks pale in comparison to the risks to retail investors from the SEC’s alliance with the crypto industry. Crypto remains unbelievably volatile. A recent selloff wiped out over $1 trillion across the crypto world. Smaller retail investors have borne the brunt of this downturn. Yet the SEC has spent the last year promoting crypto at every turn. The SEC has:

- Launched “Project Crypto,” Chair Atkins’s plan to help make the United States the “crypto capital of the world” and move America’s financial markets on-chain.

- Established a “Crypto Task Force”.

- Repealed guidance that protected customers by requiring that banks have capital to protect against the risk of loss inherent in volatile crypto assets.

- Approved the listing and trading of crypto-exchange traded products (ETPs) that are marketed to retail investors and that have suffered losses during recent market volatility.

- Approved generic listing standards for crypto ETPs so that new and untested crypto products are able to enter the market without prior SEC review or approval.

- Voted to permit the in-kind creation and redemption of crypto ETPs so that firms may create and redeem shares of crypto ETPs using crypto rather than cash.

- Issued guidance saying that SEC registered exchanges are not prohibited from facilitating the trading of certain spot crypto asset products.

- Issued guidance permitting state trust companies to act as custodians for crypto assets.

- Issued guidance stating that crypto mining activities do not involve the offer or sale of securities; that staking crypto assets does not involve the offer or sale of securities; that liquid staking does not involve the offer or sale of securities; that stablecoins do not involve the offer or sale of securities; and meme coins are not securities but rather “collectibles.”

The SEC’s guidance on meme coins is a particularly stark example of the SEC failing to protect ordinary people. Meme coins are the crypto equivalent of penny stocks in traditional securities. Both leave retail investors susceptible to pump-and-dump scams that may cause large losses. The SEC has long regulated penny stocks. Yet because meme coins involve crypto, the SEC takes the position that they are not securities and that the securities laws do not protect investors in meme coins. This means the SEC leaves meme coin investors who lose their life savings not collecting meme coins but buying them as a speculative financial asset to fend for themselves.

The SEC’s preoccupation with crypto is also especially troubling given that so few Americans care about crypto. The Federal Reserve recently published statistics that show interest in crypto is actually declining. The percentage of adults who used crypto either as an investment or as part of a financial transaction was down to 8% in 2024 from 12% in 2021. The Fed also showed that:

- Using crypto as an investment remained more common than using it for financial transactions.

- Seven percent of adults bought or held crypto as an investment in the prior 12 months.

- Two percent of adults used crypto to make a financial transaction in the prior 12 months.

The fact that the SEC would so heavily promote an industry that most Americans reject belies the assertion that the SEC is prioritizing the interests of the working man over those of Wall Street.

Enforcement

The SEC’s eagerness to cater to the crypto industry at the expense of investors extends beyond its regulatory actions. Throughout the year, the SEC dropped cases against crypto companies that were designed to compel the companies to comply with the securities laws and provide investors with the disclosures that they need to navigate an industry rife with frauds, scams, and abuses. The SEC abandoned these cases despite having previously won almost 100% of its crypto cases.

Perhaps most troubling, the SEC even dropped cases alleging fraud. In March 2023, the SEC charged crypto entrepreneur Justin Sun and three of his companies with fraudulently manipulating the secondary market for crypto asset security Tronix (TRX) through extensive wash trading. Wash trading involves the simultaneous or near-simultaneous purchase and sale of a security to falsely make it appear that there is an active market for the asset. The SEC alleged that Sun directed his employees to engage in more than 600,000 wash trades of TRX, with between 4.5 million and 7.4 million TRX wash traded daily. The SEC’s new leadership stated that it did not want the crypto markets to be a haven for fraudsters, and that its efforts to police fraud in the crypto markets would continue unabated. Still the SEC put the case on hold after Sun purchased $75 million worth of tokens issued by World Liberty Financial, President Trump’s crypto project.

The New York Times recently documented the SEC’s pullback from its crypto cases. It found:

- SEC dismissals came at a far higher rate for crypto firms. It dismissed 33% of the crypto cases initiated under the Biden administration. It dismissed only 4% of other cases.

- The SEC under Chair Atkins inherited 23 crypto cases. It retreated in 14 of them.

- The SEC has not brought a single crypto case since Chair Atkins became chair.

Unfortunately for investors, the SEC’s failure to enforce the securities laws was not limited to crypto cases. Enforcement activity overall plunged under Chair Atkins. Cornerstone Research recently published a report documenting the extent of the decline in SEC enforcement actions:

- The SEC brought 30% fewer enforcement actions against public companies and subsidiaries in fiscal year 2025 compared to fiscal year 2024.

- The SEC brought only four such cases under the new administration.

- The total amount of monetary settlements was $808 million, which was the lowest for any year in which there was a change in the administration and the second lowest since 2010.

These statistics are perhaps unsurprising given that a senior enforcement official said that the industry could expect a “more sympathetic ear” under Chair Atkins in the realm of enforcement.

Consolidated Audit Trail

Not only is the SEC reducing the number of cases that it brings but also is dismantling the most important tool it has to catch crooks. The Consolidated Audit Trail (CAT) is a tool that tracks trades in real time and allows the SEC to see the entire market. As a result, it enables the SEC to protect investors from market disruptions and stock manipulations and other predatory trading activities.

Despite its effectiveness, Chair Atkins seems intent on dismantling the CAT. The SEC has taken several actions in the past year that call the future of the CAT into question. These include:

- Directing the staff to undertake a comprehensive review of the CAT.

- Providing an exemption from the requirement to report names, addresses, and years of birth to the CAT, which makes it harder to identify the perpetrators of misconduct.

- Issuing an order reliving market participants from the need to create certain records and maintain some data in the CAT, which reduces the SEC’s insight into the market.

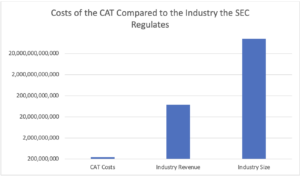

Chair Atkins justified this last order as an attempt to reduce the CAT’s costs. He decried the costs of operating the CAT, which he said were projected to exceed $248 million annually as of November 2024. This sounds expensive, and certainly some concerns about the CAT’s costs are legitimate, but the securities industry earned pre-tax net income of over $75 billion in 2024. Moreover, the SEC is responsible for overseeing capital markets that exceed $100 trillion in size.

Source: Better Markets, 2025

The costs of the CAT pale in comparison to the revenue of the industry that the SEC must regulate, as well as the size of the markets that the SEC must monitor. Understood this way, the costs of the CAT are a small price to pay for effective policing. This means the SEC must not kill the CAT.

Conclusion

The last year proves that the SEC should now be known as the Shareholder Exploitation Commission. The SEC is eliminating the fundamental safeguards that protect investors in public companies. At the same time, it is inducing investors to enter the private markets, where those safeguards do not exist at all. It is also endlessly promoting the crypto industry despite that industry’s track record of scamming retail investors and causing huge losses. The enforcement activity that is supposed to deter bad actors from preying on ordinary investors is nonexistent. And the SEC is intent on dismantling a key tool for monitoring the markets. Far from helping the workers, the SEC has spent the last year catering to the very industry that it is supposed to regulate.