One thing is clear about the banking agencies under this administration – they don’t care about community banks or the economic growth of the communities they serve. Community banks are the lifeblood of communities across America, and their financial support enables many Main Street Americans to achieve their goals and dreams through personal, home, car, and student loans, as well as loans to local small businesses and farms. Their role in communities—from coast to coast and from red state to blue state—drives broad-based growth within the real economy.

The agencies have been talking a lot about helping community banks, but that’s all it has been – just talk and no action. In fact, the actions of the agencies over the past year are harming community banks because they are almost entirely focused on benefiting the biggest Wall Street banks. Community banks already face an unlevel playing field that’s tipped heavily in favor of big banks, leaving community banks struggling to keep up and allowing the big banks to gain more and more market share. The agencies’ recent policies are making this much worse.

Their policies are also bad for the economic growth of Main Street Americans because community banks are much more supportive of Main Street businesses, households, and farms than large banks. Put simply, big banks getting bigger means less support for Main Street. This is obvious when looking at the data – compared to large banks, community banks:

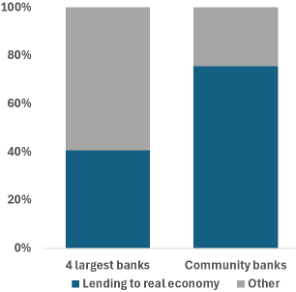

- Use 75 percent of their deposits for direct lending to the real economy, compared to the largest banks that use only 40 percent of their deposits for real-economy lending[1]

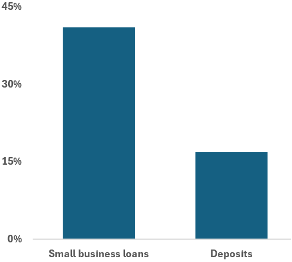

- Lend to a broader range of borrowers through their unique “relationship banking” model, especially with small businesses for which community banks hold around 40 percent of balances of small business loans[2]

- Provide more support to communities during economic downturns.

Percentage of deposits used for direct lending to the real economy

Community bank shares of small business loans by balance and deposits

The largest, most complex banks should have the strongest regulations – much stronger than for community banks – because they engage in the riskiest activities, like trading and derivatives, and pose substantial risk to the banking system and financial stability. This need for strong regulations has been proven repeatedly by the reckless actions of big banks that resulted in the catastrophic 2008 crash, when tens of millions of Main Street Americans lost their jobs, homes, and savings, and the 2023 regional bank crisis, when three of the largest bank failures in history happened.

Despite these facts, the agencies are engaged in upside-down policymaking in which the largest banks ultimately will have the same or, in important areas, even less regulation than community banks. For example, JP Morgan – a financial conglomerate with $4.5 trillion in assets – has a leverage capital requirement that is about half the requirement of many community banks, which generally have less than $10 billion in assets. This allows large banks to take on more risks, make more profits, and take more market share from community banks.

This only ends one way: big banks will become even bigger and gain more market share from the community banks, resulting in more lending to large corporations and the wealthy and less lending to Main Street borrowers, especially small businesses. This fact sheet summarizes how the actions of the banking agencies are widening the gross advantage of the largest banks, hurting community banks and Main Street economic growth.

Capital Requirements for the Largest, Most Complex Banks Are Close to or Less Than Capital Requirements for Community Banks

The most obvious advantage the largest banks have over community banks is with capital requirements. Strong levels of capital funding are essential for banks because they protect banks from failure by absorbing losses while also being used to fund financial activities, such as making loans. The biggest banks that engage in the riskiest activities must have the highest capital requirements to protect against those risks and the great risk they pose to the banking system and financial stability.

But big banks have been pushing for lower and lower capital requirements because that increases their profits and executive bonuses, which they prioritize over supporting the real economy. The banking agencies under this administration are giving them exactly what they want and are greatly reducing their capital requirements back to the dangerously low levels they had just before the 2008 crash. The lower the amount of capital a bank has, the higher the profits, stock price, and bonuses for the CEO and executives. That’s exactly how JPMorgan Chase CEO Jamie Dimon just pocketed $770 million.

Big banks would rather have less capital so that they can make more profits in good times at the expense of limiting economic support during bad times or – in the worst case – putting the expense on taxpayers when they fail. Put simply, sufficient capital is good for economic growth because it means banks can support the economy in good times and bad.

That is why community banks have done more lending in past recessions than large banks – they have higher capital levels, a clear indication that they prioritize supporting the real economy over profits. Their lending has prevented communities from experiencing the worst of recessions and – in some cases – even supported growth in communities while others suffered. Community banks also do relatively more lending in good times, especially to the small businesses that create wealth for many in communities across America.

Instead of supporting the mission of community banks, the agencies’ actions over the last year add up to an upside-down capital requirement framework where the largest banks have the lowest capital requirements. The upside-down framework can be seen most clearly through the so-called leverage capital requirements, because leverage is a straightforward measure of capital levels. It can be thought of simply as the maximum percentage of losses a bank can take across its financial activities before it fails.

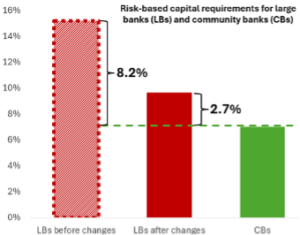

Leverage capital requirements for large banks (LBs) and community banks (CBs)

Note: Community banks can opt in to the community bank leverage ratio (CBLR) framework, for which different standards apply, or remain under the standard capital requirement framework.

Collectively, the largest, most complex banks have a leverage requirement of around 3.8 percent, meaning they can take only 3.8 percent of losses before they fail. This large bank requirement is less than half the proposed 8 percent requirement that will apply to many community banks. Even the original large bank leverage requirement of 5 percent, before the recent deregulation, was much lower. Other community banks use a different, lower leverage requirement of 4 percent, but that is still higher than the current requirement for the largest banks. In either case, the largest banks with trillions of dollars in assets have lower leverage capital requirements than community banks with less than $10 billion in assets.

There are also risk-based requirements, which are based on the “riskiness” of specific financial activities. After all the deregulatory changes are implemented by the agencies to those requirements, there will be little difference between the requirements for the largest banks and community banks. The difference between the two requirements historically has been much bigger, which is how it should be considering how much more risk a $4.5 trillion bank like JPMorgan Chase poses to the financial system than a $1 billion community bank. As the name suggests, risk-based requirements should be significantly higher for banks that present more risk to themselves and to the system.

The agencies are also seeking to lower the capital required specifically for the most profitable and riskiest activities of large banks – trading and derivatives. Bloomberg reported that an expected proposal on risk-based capital requirements likely would do exactly that: “[banks] that have bigger trading portfolios could see less of an increase – or even a decrease” in their risk-based capital requirements. This means those activities will become even more profitable, creating a stronger incentive for the biggest banks to do more of those activities and less lending to the real economy.

This all adds up to a huge advantage for the largest banks. By avoiding the upfront cost of having enough capital and instead passing that cost onto the public, the largest banks can have massive growth in profits. Considering their size, their profits add up to a lot of money – over $120 billion last year just for the four largest banks. And with those huge profits, they can – and do – things to gain more and more market share that smaller banks with strong levels of capital can’t.

They can undercut their competition or buy up their smaller competitors, including community banks, to take over markets. They also spend the money on enhancements to their business models, such as technological improvements, to bring in more customers. This leaves community banks struggling to compete in many markets and unable to keep pace with the largest banks on the latest business enhancements. As capital requirements are lowered further by the agencies, this competitive advantage will only get worse and big banks will only get bigger.

Supervision of the Biggest Banks Has Been Weakened to Be Almost the Same as for Community Banks, Harming Economic Growth

Banks are supervised by the banking agencies to make sure they don’t misuse depositors’ money, break the law, or engage in high-risk activities. The strongest supervision must apply to the largest banks because their distress or failure results in large losses, catastrophic crashes, taxpayer bailouts, and economic calamity for the country. Big banks repeatedly have taken big risks that have brought about such disastrous consequences, for example:

- In 2008, when tens of millions of Main Street Americans lost their jobs, homes, and savings due to the catastrophic 2008 crash caused by the risk-taking of Wall Street’s biggest financial firms

- At JP Morgan in 2013, when reckless actions and failures in risk management resulted in $6 billion “London Whale” trading losses.

- In 2021, when $10 billion of losses across multiple banks resulted from widespread failures in basic risk management around the failed Archegos family fund.

Despite this history, the banking agencies have taken actions that weaken the supervision of large banks to the point where there is little difference between their supervision and that of community banks. In fact, that is a stated goal of the agencies. For example, one key objective in a recent proposal from the Federal Reserve was to “further align” the supervisory framework for large banks with the frameworks used for smaller banks.

When supervision is weakened, the agencies keep less of an eye on risk-taking, and so there is no doubt risk taking by big banks will increase as they look for bigger profits and bonuses. For example, excessive risk-taking is how Wall Street banks were passing out $100 million bonuses to traders before the 2008 crash, when supervision was very weak.

In addition to failures and bailouts, weak supervision and excess risk-taking by big banks are bad for economic growth. First, the way banks take on a lot of risk is by redirecting financial resources away from activities that support durable growth in the real economy towards risky activities in financial markets and to those that lead to the type of bubble growth that results in economic crashes and harm to Main Street households. For example, before the 2008 crash, big banks were trading ultra-risky derivatives and originating loans to borrowers that could not afford them.

Second, weak supervision of big banks harms community banks and the communities they support by widening the already-huge disadvantages they face compared to big banks. Just as with the reduction in big bank capital requirements, if big banks are not properly supervised, they can take bigger risks and increase their profits while putting the costs of losses and failures on the American public. These increased profits are used to gain market share and shut out competitors, especially smaller competitors like community banks.

Conclusion

It is clear that the banking agencies don’t care about community banks and instead are focused on delivering everything Wall Street wants. Nearly all the actions the agencies have taken over the last year have greatly benefited big banks, which should have the strongest regulations and supervision. Instead, after the agencies complete their deregulatory actions, the biggest banks will have a regulation and supervision framework that is similar to – and in some cases shockingly less strict than – the framework for community banks.

This is bad for the economic growth of Main Street because it will widen the already-huge advantage big banks have over community banks, resulting in greater concentration of the banking system and less support for Main Street small businesses, households, and farms. There is no financial institution that supports our communities and broad-based economic growth more than our community banks. The banking agencies must turn their upside-down policy framework right side-up and support our community banks as much as they support our economy.

[1] Analysis based on deposit data from Call Report.

[2] Analysis based on the number and balance of small business loans as defined in schedule RC-C Part II of the Call Report.