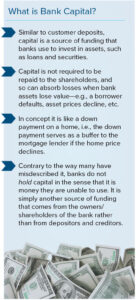

The largest banks in the U.S. remain subject to insufficient capital requirements that undermine the stability of the financial system and leave the possibility of future banking crises too high. Capital standards must be strengthened to fully support the benefits to society that come from a strong and resilient banking system, especially during period of financial and economic stress. None of the industry’s arguments against higher requirements are supported by real-life experience or research, while the costs of insufficient capital requirements has been real and devastating for the American people. Capital requirements were irresponsibly low prior to the 2008 Crash, resulting in bank failures, massive taxpayer bailouts, and a catastrophic financial and economic collapse with a $20 trillion impact to the economy.

The largest banks in the U.S. remain subject to insufficient capital requirements that undermine the stability of the financial system and leave the possibility of future banking crises too high. Capital standards must be strengthened to fully support the benefits to society that come from a strong and resilient banking system, especially during period of financial and economic stress. None of the industry’s arguments against higher requirements are supported by real-life experience or research, while the costs of insufficient capital requirements has been real and devastating for the American people. Capital requirements were irresponsibly low prior to the 2008 Crash, resulting in bank failures, massive taxpayer bailouts, and a catastrophic financial and economic collapse with a $20 trillion impact to the economy.

It’s clear that capital requirements must be strengthened for our largest banks, and that this would benefit the American people. Our report discusses the reasons those requirements must be increased, the baselessness of industry talking points, and two key aspects in which the capital framework must be strengthened.

Industry Arguments Against Higher Capital Requirements Are Wrong

The banking industry’s main public argument against higher capital requirements is the claim that this would force them to reduce lending or greatly increase the cost of credit, thus harming economic growth. This argument was repeated by the CEOs of the largest banks in the U.S. in hearings this year before Congress.

The reality is there is no real-life evidence of this. In fact, according to data from the Bank for International Settlements, both the amount of lending and the share of lending coming from banks to the non-financial sector has actually increased between 2013, when higher capital requirements started taking effect, and the 2020 pandemic.

Other industry arguments have been shown to be wrong:

- Banks claimed they were a “source of strength” during the 2020 pandemic-related market stress when in fact, they benefited massively from trillions of dollars of support from the Fed and Congress.

- Higher capital levels reduce the overall cost of capital by as much as 50%.

- U.S. banks have outperformed their European counterparts despite having higher requirements.

- Financial activities and risks in the shadow banking financial sector are an argument for more capital at banks not less.

Capital Requirements Must be Stronger

The argument for higher capital requirements is simple and obvious: better capitalized banks create a stronger, more resilient, and stable financial system that is less likely to cause or exacerbate economic and financial downturns. When large banks are undercapitalized, such downturns are not only more likely, but also more likely to become severe financial and economic crises that can cause tremendous harm to Americans from coast-to-coast and lead to taxpayer-funded bailouts. Additionally, research shows that higher bank capital “significantly lower[s] the cost of a crisis by sustaining bank lending during the resulting recession.”

Many estimates from academics and regulatory organizations of optimal capital requirements indicate that substantially stronger capital standards are both necessary and would be beneficial:

- The Federal Reserve Bank of Minneapolis estimates capital requirements should be 23.5% of risk-weighted assets and 15% of total assets.

- Federal Reserve Board analysis showed the most severe loss of a bank holding company during the 2008 Crash was 19% of risk weighted assets.

- Economists at the International Monetary Fund estimated capital requirements should be 23% of risk-weighted assets.

- Economists Anat Admati and Martin Hellwig, in their 2013 book The Banker’s New Clothes, estimated capital leverage requirements of at least 20% – 30% of total assets.

- The Basel Committee on Banking Supervision (BCBS), in a 2010 paper, estimated risk-based capital requirements of 16% would be appropriate.

There are two parts of the framework whose strength must be a priority: (1) the Federal Reserve supervisory stress test, which is the basis for the most important and binding U.S. large bank capital requirements, and (2) any potential Basel Endgame modifications, which must not be driven by a goal (that has been misguidedly promoted by many) to maintain capital requirements at approximately the same level as those currently in place. These are discussed in more detail in our report.

Learn more in our full Report or download this Fact Sheet on strengthening capital requirements.