Introduction

Investors in private credit funds can’t get out fast enough. These funds normally impose a limit on redemptions of 5% per quarter. But given the recent turmoil in private credit, investor redemption requests in many funds have far exceeded this limit. Some funds have raised the 5% limit to accommodate the flood of redemption requests. Others have enforced the 5% limit. Either way, the evidence is that investors who find themselves in private credit now can’t wait to get out.

Source: The Wall Street Journal

The private funds industry says that the concerns animating this exodus from private credit are overblown. It seems that investors disagree. What is certain, though, is that now is exactly the wrong time to expose retail investors to private credit and other risky alternative investments.

Yet that is exactly what the Department of Labor (DOL) intends to do. Yesterday, the comment period ended on DOL’s proposal to facilitate the inclusion of alternative investments such as private credit in millions of Americans’ 401(k) plans. The events of the past few months reveal that there could hardly be a proposal more dangerous to Americans’ retirement security.

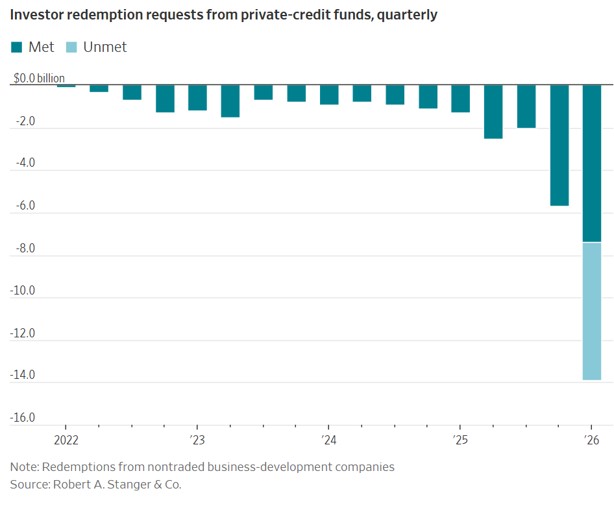

Investors Are Trapped in Private Credit Funds

Although private credit funds have experienced turmoil for a while now, the events of the last few months have made the risks of private credit impossible to ignore. In that time, it has become clear that investors in private credit funds want to, but are not always able to, get their money back.

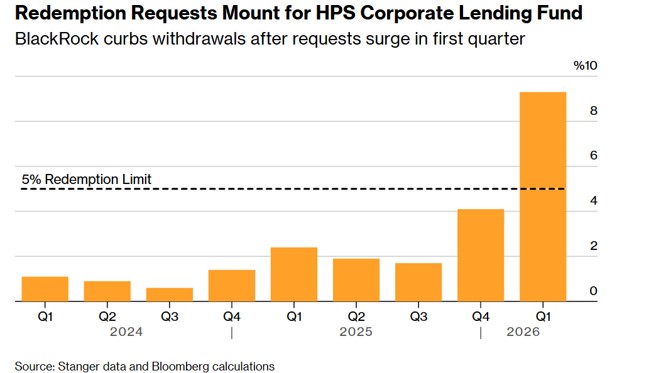

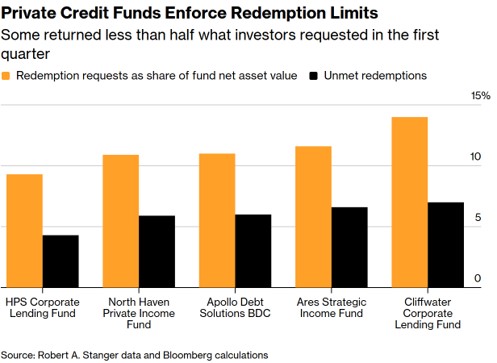

Some of the biggest names in private credit have enforced the 5% cap on redemption requests, meaning that for the time being investors in these funds are essentially trapped.

- Shareholders in a BlackRock private credit fund requested 9.3% of their shares, but BlackRock determined to cap redemptions at 5%. This meant that investors requested $1.2 billion in value back but received only $620 million. These redemption requests far exceeded the redemption requests that the fund received over the past two years.

- Morgan Stanley also capped redemptions in one of its private credit funds at 5%, which meant investors received less than half of the money they sought to withdraw from the fund.

- Apollo Global Management similarly capped redemptions in one of its largest private credit funds at 5%, even though clients sought to redeem 11.2% of their invested capital.

- Ares Management also capped redemptions at 5% after receiving requests of about 11.6%.

- Carlye Group received redemption requests of 15.7% but capped redemptions at 5%, meaning investors received only $240 million of the $750 million they requested.

- Blue Owl capped redemptions at 5% in two of its private credit funds after investors sought to pull $5.4 billion from the funds—22% of one fund and 41% of a second fund.

Other firms have allowed investors to exceed the 5% cap, but even that has not always been enough for investors to receive back all of the money that they have requested.

- Blackstone raised the 5% limit on redemptions to accommodate redemption requests of 7.9%, or about $3.8 billion, in its flagship private credit fund.

- Oaktree Capital Management allowed investors to take out 8.5% of the assets, or about $400 million, from one of its private credit funds instead of enforcing the 5% cap.

- Cliffwater allowed redemptions of 7% from its flagship private credit fund, but that was still only half of the record 14% redemption requests that it received.

Overall, investors sought to pull $20 billion from private credit funds in the first quarter of the year.

Source: Bloomberg

The Industry Itself Seems to Recognize the Problems with Private Credit

Investors are understandably upset about their inability to access their money, and this has caused something of a reckoning in the private funds industry.

- Jim Zetler, Apollo’s president, said in March that the industry may have failed to clearly explain liquidity restrictions to investors now seeking to redeem their funds.

- Doug Ostrover, co-chief executive officer of Blue Owl, amplified this point:

“Between us, and the advisers who sell our products, I don’t think we made it clear enough,” [Ostrover] told a conference in Australia.

- John Waldron, Goldman Sach’s president and chief operating officer, said in April that some private credit managers had mispresented the liquidity of their funds:

“Not everybody has marketed their product as clearly as, certainly we would like to see with the clarity that this is really not a liquid product. It’s not semi-liquid. It’s really illiquid.” Waldron said. “Those retail investors, I think have the perception of more liquidity than is the reality.”

The financial industry also seems to recognize that the turmoil is here to stay.

- In April, the Wall Street Journal reported that “Morgan Stanley analysis laid out a dour future for the industry . . . saying they expect loan defaults to increase, fundraising to be sluggish and returns to disappoint. ‘In a nutshell, we think risks in private credit are significant,’ the analysts wrote.”

- Later that month, the Wall Street Journal further reported that large banks “are preparing to offer a new way for investors to bet against managers of private credit funds. . . . Hedge funds are keen for a way to easily make bets on a downturn in private credit. Stress has been building, as a spate of defaults and losses . . . caused a stampede of individual investors asking for their money back.”

- Zetler, of Apollo, said in May that he expects wealthy individuals to keep trying to withdraw their money from some private credit funds after several months of outflows from the vehicles. ‘I don’t think it was a one-shot,’ Zetler said.

Perhaps most significantly, federal prosecutors are now scrutinizing the valuation practices at a BlackRock private credit fund. Skepticism about private credit valuations is one of the reasons investors began to ask managers for their money back en masse. It would be an understatement to say that this seems like a terrible time to expose retail investors to private credit.

Now is Not the Time to Expose Retail Investors to Private Credit

Nonetheless, the DOL has decided that now is the time to try to induce plan sponsors to include private credit and other alternative assets in the 401(k)s of millions of American investors. DOL says that its proposal will “democratize access to alternative investments” and “increase potential retirement options” for individuals with 401(k)s, as if these individuals seek investment options in their 401(k)s that include private credit. Nothing could be further from the truth.

The fact is that numerous surveys show that retail investors do not want private credit and other alternative investments in the options of investments for their 401(k)s. Given this turmoil in private credit, it is unsurprising that retail investors are not clamoring for their inclusion. The perspective of Michelle Singletary, who writes about finance for the Washington Post, is illuminating. She says:

“I have talked to hundreds of workers investing in their workplace plans, and I have never, ever heard a single person complain that they didn’t have access to alternative assets.”

It should therefore also be unsurprising that these workers do not stand to benefit from the inclusion of private market assets in their 401(k)s. Research increasingly shows that private markets underperform public markets. This means that the beneficiaries of DOL’s plan will not be American workers but the firms who stand to profit from selling these workers private funds:

For the private credit industry, access to retirement savers and fewer restrictions on trading can’t come soon enough. Firms including Apollo, Blackstone, Carlyle Group Inc. and Blue Owl Capital Inc. are grappling with a surge in redemption requests from funds aimed at retail investors; an influx of cash from retirement plans could help stem the outflows.

But the fact that the spigot is running dry with respect to investors already in private credit is no reason to allow private funds to access the retirement savings in Americans’ 401(k)s. Simply because the industry wants access to those savings accounts does not mean it should have it.

“Workers aren’t saying, ‘This is what we want,’” said Renée M. Jones, a professor at Boston College Law School with a forthcoming book, “Untamed Unicorns: Why Startup Finance is Broken and How to Fix It.” “It’s more of the industry saying, ‘This is what you should have.’”

There’s no question that Wall Street is salivating over DOL’s proposal. That should be a red flag, not a green light. Investors currently in private credit are running for the hills, and private credit funds need retail investors to plug the gap. But retail investors don’t need private credit funds. The $12 trillion in workers’ 401(k)s does not exist to bail out private credit. It exists for Americans’ retirement. DOL should not endanger Americans’ savings for the sake of private credit funds.

Conclusion

We filed a comment letter with DOL highlighting the turmoil in private credit and arguing that now is not the time to expose retail investors to private credit funds. We expect others did the same. Now that the comment period has closed, we look forward to reviewing the comment file. If, as we expect, other commenters also objected to the proposal, we hope that DOL will have the good sense to withdraw it. The retirement security of millions of Americans is at stake. Investors in private credit are currently fleeing private credit funds, and many can’t get out fast enough. DOL should want to prevent millions of Americans with 401(k)s from one day having to do the same.