There is a long history in the U.S. of ensuring the separation between banking and commerce, and for good reason. The Bank Holding Company Act, passed in 1956, prohibits bank holding companies from engaging in commercial activities and from controlling (or being controlled by) commercial enterprises. This longstanding policy was specifically designed to prevent the dangers associated with banking-and-commercial conglomerates, including:

- Excessive concentrations of financial and economic power and political influence;

- Conflicts of interest that would compromise the ability of banks to act as objective providers of credit and other financial services; and

- Heightened risk of contagion between the financial and commercial sectors of our economy, greatly increasing the likelihood of systemic crises that would require huge bailouts to avoid devastating financial, economic, and social consequences.

Simply put, Congress has consistently recognized that commercial enterprises should not benefit from the backstop provided to the tightly-regulated banking system.

However, the existence of industrial loan companies (“ILCs” or “corporate banks”) directly contradicts this separation, allowing regular commercial companies to own and operate banks. These corporate banks are allowed to exist because of a little-known loophole that allows corporations not only to own banks but also to do so without the same regulations as “traditional” banks. In other words, this special carveout provides corporate banks with an unfair advantage and increases the type of risks that the separation of commerce and banking seeks to avoid.

Holding companies that own depository institutions (e.g., JP Morgan, which owns Chase Banks) are regulated and supervised by the Federal Reserve (“Fed”), but the ILC exception allows certain bank-owning commercial corporations to evade Fed supervision of their parent company. Today, corporate banks are owned by a variety of corporate giants, such as auto companies BMW and Toyota, the fintech company Square, and the office supply and shipping company Pitney Bowes. And with the expectation of a lax approval process under the current administration, many more companies are lining up to start corporate banks.

The proliferation of corporate banks without parent company oversight and supervision stands to create severe consequences for both the financial system and Americans at large. Supervision of the parent companies of banks, especially large banks, is essential. Parent companies are relied upon as sources of strength for banks; having no supervision or visibility into the parent companies of corporate banks creates a dangerous blind spot. Moreover, corporate banks foster unfair competition, conflicts of interest, and even potentially weaker risk management because of their deep linkages to retail corporations. For example, a corporate bank that is a subsidiary of an auto company is incentivized to make more auto loans to sell more vehicles. This could be achieved by lowering risk management standards to allow more customers to qualify for loans that traditional banks with higher risk management standards would not make, directly leading to more auto sales for the parent company. At the end of the day, looser regulation of corporate banks, and a complete lack of regulation of their parent companies, puts the financial system and all Americans at heightened risk of failures and bailouts.

Recent Regulatory Developments

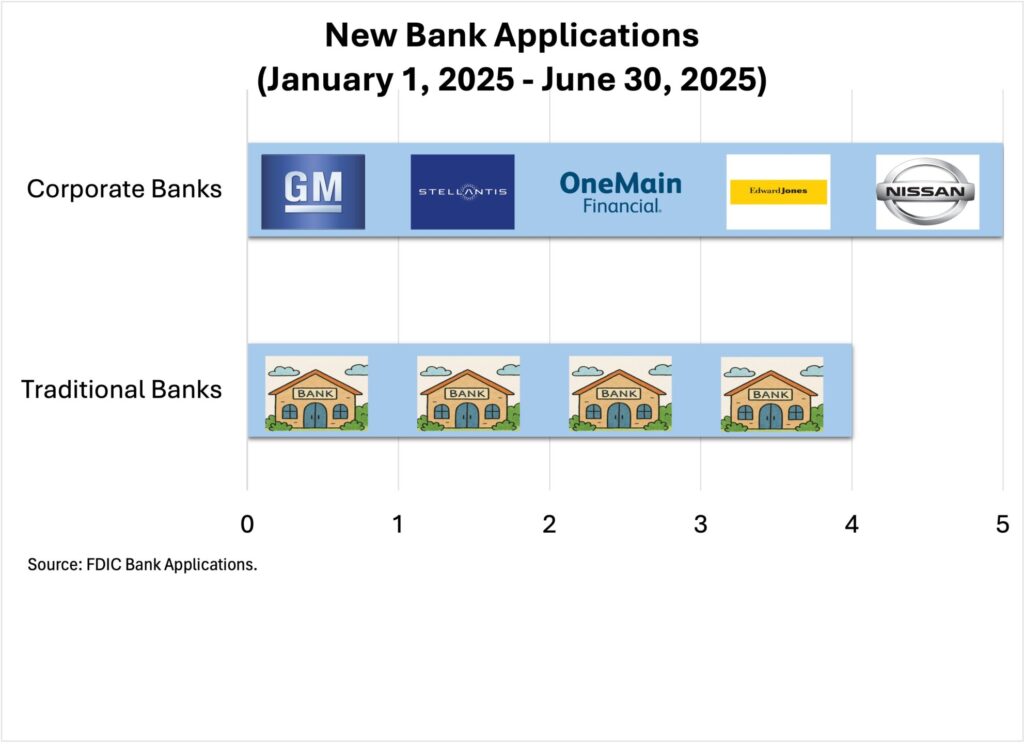

In 2024, the Federal Deposit Insurance Corporation (“FDIC”) rightly recognized the risks that corporate banks present to Main Street, the economy, and financial stability. The FDIC proposed a rule, which Better Markets supported, that would take much-needed action to strengthen regulatory control of corporate banks and protect the financial system. Unfortunately, the FDIC’s then-Vice Chairman Travis Hill opposed the proposal. In July 2025, the proposed rule was rescinded after Hill became Acting Chair. Among his policy priorities, Hill included opening more corporate banks as a key component of the larger goal of opening more new banks throughout the country. This invitation led to five applications to open new corporate banks in the first half of 2025 alone, outnumbering the applications for new traditional banks during the same period (see Chart 1). This trend contrasts with the 23 applications for new traditional banks received by the FDIC in 2023 and 2024 combined, none of which were corporate banks. This shift should concern all Americans because the FDIC should be supporting community banks and Main Street. Instead, it is disproportionately supporting corporate giants and endangering financial stability.

Chart 1

The bottom line is that the American people deserve comprehensive regulatory guardrails around corporate banks. The health of the economy and financial system requires strong regulation of all types of banking. This fact sheet details how the lack of proper supervision and regulation of corporate banks results in risks that are difficult to identify, quantify, and control. The existing regulatory frameworks for these institutions primarily benefit the handful of commercial enterprises that are affiliated with corporate banks. They must change to prioritize and protect Main Street America and financial stability.

Background

History of Corporate Banks

Corporate banks began in the early 1900s as small, state-chartered loan companies. Early corporate banks made small loans to factory workers and others with low or moderate incomes. However, corporate banks have grown substantially from their humble beginnings, both in asset size and complexity, and they are no longer focused on serving factory workers and others with low or moderate incomes.

In 2025, corporate banks had more than $230 billion in total assets. The largest corporate bank—UBS Bank USA—had more than $116 billion in total assets as of March 31, 2025, making it larger than Signature Bank, which required a systemic risk exception to protect the financial system when it failed in March 2023. UBS Bank USA describes itself as “dedicated to serving the deposit and borrowing needs of affluent and high net worth investors,” a mission that is clearly not aligned with supporting everyday consumers on Main Street.

Corporate banks have experienced tremendous growth in complexity, variety, and size. In part, this growth stems from Congress creating special rules for corporate banks in 1987 with the Competitive Equality Banking Act (“CEBA”), which excluded corporate banks from the “bank” definition and from the general prohibition against the acquisition of banks by enterprises that fall outside the bank holding company framework.

Some of the most notable and controversial examples of corporate banks are Wal-Mart’s and Home Depot’s attempts to become corporate banks. These application received widespread opposition from community bankers, public interest groups, other retailers, regulators, labor unions, and members of Congress citing an array of problems ranging from concerns that the corporate bank would soon grow large enough that it would be too big to fail, threaten financial stability, and become a taxpayer liability if it got into financial trouble. Moreover, its direct access to the payments system would represent a competitive advantage relative to other retail stores.

Recent Expansion of Corporate Bank Applications

One of the goals of Acting FDIC Chairman Hill is to increase new bank formation. Hill said that the formation of new banks has “fallen off a cliff” and has indicated an openness to new corporate banks as one way to fill this void, a strange solution since corporate banks are not regular banks. In the first half of 2025, five corporate banks submitted applications with the FDIC to open, including:

- GM Financial Bank: would provide auto loans to customers for purchases of GM vehicles.

- Stellantis Bank USA: would provide auto loans for Stellantis customers, including buyers of Chrysler, Fiat, and Jeep vehicles, and many others.

- Nissan Bank U.S., LLC: would provide auto loans for buyers of Nissan and Infiniti vehicles, and other brands.

- Edward Jones Bank: would provide financing to increase sales of Edward Jones’ financial products.

- One Main Bank: would provide personal loans, auto loans, credit card loans, and other financial products to support One Main Financial, a finance company with a history of deceptive sales practices.

Risks of Corporate Banks

The FDIC itself, along with banking industry trade groups such as the Independent Community Bankers of America (“ICBA”) and consumer protection organizations such as the National Community Reinvestment Coalition (“NCRC”), have detailed many serious risks associated with corporate banks.

These risks fit broadly into three categories:

- Supervisory Concerns: Substantial reliance on a parent company or affiliate makes corporate banks vulnerable to financial distress or operational disruptions at the parent. In other words, if the parent company needs money, it may siphon assets from its subsidiaries, including the corporate bank, which would weaken the financial position of the corporate bank.

- Convenience and Needs Concerns: Corporate banks are inherently dependent and focused on the parent company’s business lines and customers. This narrow focus conflicts with the public purpose of banks, which are expected to serve the convenience and needs of the community broadly. Corporate banks that serve niche markets and only exist to serve consumers who purchase a specific product sold by the parent company raise fundamental questions about the social benefit of corporate banks.

- Failure Concerns: Failures of a corporate bank are difficult, lengthy, and costly, compared to traditional banks, because of corporate banks’ narrow business lines that are often entirely focused on supporting the corporate activities of the parent company. In other words, it is unlikely that a traditional bank could easily acquire a failed corporate bank and seamlessly integrate it into the traditional bank’s existing operating structure. This lack of “franchise value” could cause the FDIC to have to utilize resolution mechanisms that are more costly to the FDIC’s Deposit Insurance Fund (“DIF”) and potentially to taxpayers.

Data on the cost of bank failures support these concerns. While there have been fewer corporate bank failures than traditional bank failures, simply because there are only a handful of corporate banks compared to thousands of traditional banks, the loss rates for corporate banks that do fail are much higher, nearly double the rate for other banks. For example, between 1986 and 2017, the loss rate—the cost to the DIF relative to the total assets of the failed bank—for the 23 corporate banks that failed was nearly 25%, compared to the loss rate of only 13% for other banks. This demonstrates that corporate banks present more risk to the DIF and taxpayers than traditional banks, and should therefore be supervised more strictly and prudently, not given additional leniency.

The FDIC recognizes these risks and, in its 2024 proposed rule, detailed experience and examples to underscore the serious challenges with corporate banks:

The FDIC’s experience during the 2008-2009 Financial Crisis showed that business models involving an insured depository institution (IDI) inextricably tied to and reliant on the parent and/or its affiliates creates significant challenges and risks to the DIF, especially in circumstances where the parent organization experiences financial stress and/or declares bankruptcy. Where an industrial bank is significantly reliant on and interconnected with its parent organization to generate business on both sides of the balance sheet (e.g., for funding and for lending), as well as operational systems and support, financial difficulties at the parent organization could be transmitted to the dependent industrial bank. Such a captive model creates material concerns about the viability of the industrial bank’s proposed business model on a standalone basis and the industrial bank’s franchise value in the event the parent organization experiences financial difficulty or failure.

Furthermore, the FDIC explains how the corporate bank business model causes problems and increases costs in the resolution process:

In some industrial bank proposals that the FDIC has received, the viability and operations of the bank are dependent on ongoing support from the parent organization. In such cases, financial or operational stress at the parent company or any of its affiliates reduces the franchise value of the industrial bank in the event of failure and complicates its resolution. The underlying value of such an industrial bank lies in its connection with the parent organization, which may provide benefits including, but not limited to, name recognition, clients or referrals, personnel and back-office support, and/or specific product offerings that complement the parent company’s or affiliates’ lines of business. If such connections were to be severed, the FDIC likely would find it more difficult to facilitate a resolution with a healthy bank, and it likely would be forced to employ less efficient resolution methods that are more lengthy, cumbersome, and costly, such as depositor payouts and piecemeal loan (or other asset) sales.

Similarly, the loss of critical support services previously provided to the industrial bank by its parent organization or affiliates would pose a potentially significant challenge in a resolution scenario, as the parent or affiliated entities may no longer be able to fulfill their obligations under existing service agreements. . . . If such arrangements are terminated, the industrial bank’s franchise value would be significantly diminished. This situation could leave the FDIC in a position where it has no choice but to conduct resolution methods that are more disruptive and expensive.

The ICBA focuses on the inherent conflict of interest that exists with corporate banks that cannot “function as neutral arbiters of credit,” which would directly support the business model of the parent company. It also underscores the risks to the DIF and the propagation of systemic risks that will cause widespread harm to the banking system financial system, and the economy at large.

The NCRC shares these concerns and adds fair lending concerns related to recent corporate bank applications (for example, see here, here, and here). The NCRC explains how corporate banks do not have community reinvestment areas that are commensurate with the area in which they do business. Corporate bank operations are often national in scope, or at least include several states, but their community reinvestment obligations only apply to the immediate area around their physical headquarters location, most commonly in Utah.

Recommendations

On July 15, 2025, the FDIC took a step in the wrong direction with its withdrawal of the rulemaking proposal that would have strengthened regulatory controls around corporate banks. Acting Chairman Hill stated that he wants to start “with a clean sheet of paper and [solicit] feedback in a more open-ended way.” This action simply doesn’t make sense. It can only be seen as a concession to the corporations that want to open corporate banks and existing corporate banks looking to maintain existing loopholes in the rules. Conversely, every other entity from the banking industry, to public interest groups representing consumers, and even the FDIC itself, has identified a long list of serious risks related to corporate banks that point toward taking action that protect society against corporate banks.

The FDIC must prioritize the protection of the financial system and Main Street Americans from the risks, instability, and cost of corporate banks with the following actions:

- Fully close the loophole that permits commercial firms to own and control corporate banks. The FDIC should impose a new moratorium on corporate bank applications and urge Congress to close the statutory loophole by exempting these banks and their parent companies from the supervisory framework that is normally applicable to bank holding companies. That supervisory framework is ill-equipped to supervise commercial firms, nor was it ever intended to do so.

We recognize that the loophole cannot be closed immediately, so in the meantime, we recommend that the FDIC:

- Strengthen the regulations that apply to corporations that own corporate banks. In its 2024 proposal, the FDIC had considered stronger rules for new corporate banks but had not taken the consideration far enough because it planned to exempt existing corporate banks from the stronger rules. This is the equivalent of allowing drivers who are now known to be dangerous and a threat to the public to continue to drive on the roads because they have an existing license, or allowing medications that are now known to be harmful to continue to be prescribed simply because they were once thought to be effective. Just because in the past something was not recognized or well understood by regulators does not mean it is OK to continue once the elevated risks are known. Moreover, the fact that existing corporate banks are currently in satisfactory financial condition does not insulate them forever from the known problems that may stem from their inherent characteristics and vulnerabilities.

- Commit to holding a public hearing and soliciting public comments related to the convenience and needs of the community for every corporate bank application. The FDIC has rightly identified the challenges that corporate banks inherently face in meeting the convenience and needs of the broader community, given their narrow focus on a certain set of customers or business lines. The FDIC has also correctly stated that the benefits of a corporate bank are likely to accrue to the parent company rather than the community. These facts point to the need for a comprehensive assessment of the ability of corporate banks to serve the community broadly and the potential negative consequences of approval for every potential new corporate bank.