The Community Reinvestment Act (CRA) was intended to improve access to credit, investment and banking services for historically underserved individuals and communities. But for far too many Americans, the promises of the CRA have remained unfulfilled. Homeownership rates have remained stagnant, wealth gaps have grown, and a significant proportion of American society remains un- or under-banked. These deficits are disproportionately large among Black and Hispanic households.

Better Markets’ comment letter to the Federal Reserve, OCC, and FDIC, discusses the failures of the current CRA implementation, the agencies’ proposal to attempt to strengthen and modernize the CRA rule, and how that proposal must be improved and expanded to ensure the law’s mandates are achieved through robust supervision as well as greater measurability and transparency.

Shortcomings of the CRA

In the more than 40 years since the CRA was enacted and 25 years since its implementing rules have been materially updated, the CRA still has not fulfilled its promise. Its current implementation practices and procedures have allowed for too much discretion in CRA assessments and too little transparency, oversight, and accountability.

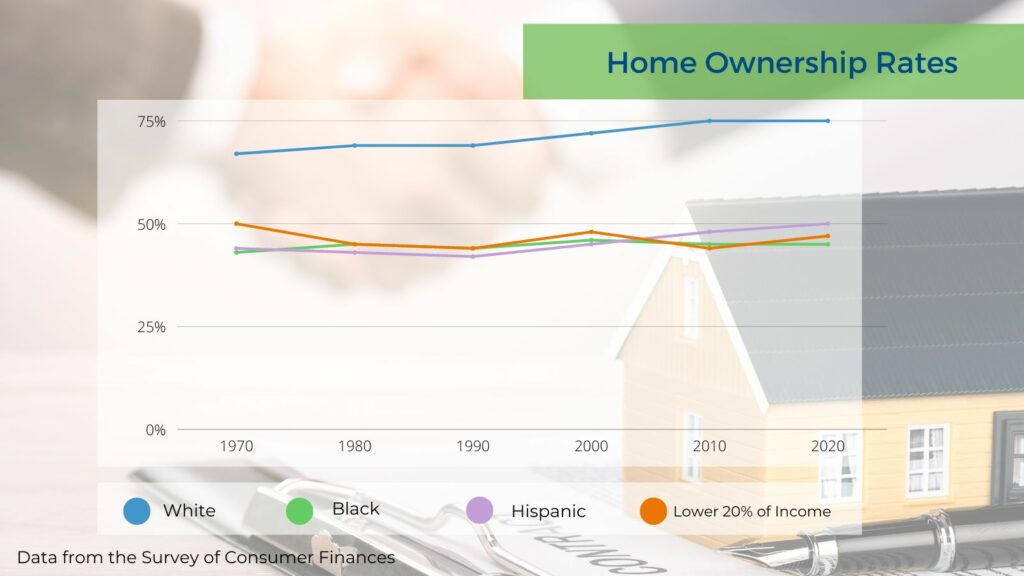

Two shocking statistics highlight the gross disparity in the way the CRA is implemented (bank focused) and how it fails to achieve the actual goals of the CRA (people focused): despite 98% of banks passing their CRA examinations, home ownership rates among the lowest income earners and Black and Hispanic Americans are no greater today than they were when the CRA was passed into law, and these rates remain well below those for higher-income and white Americans.

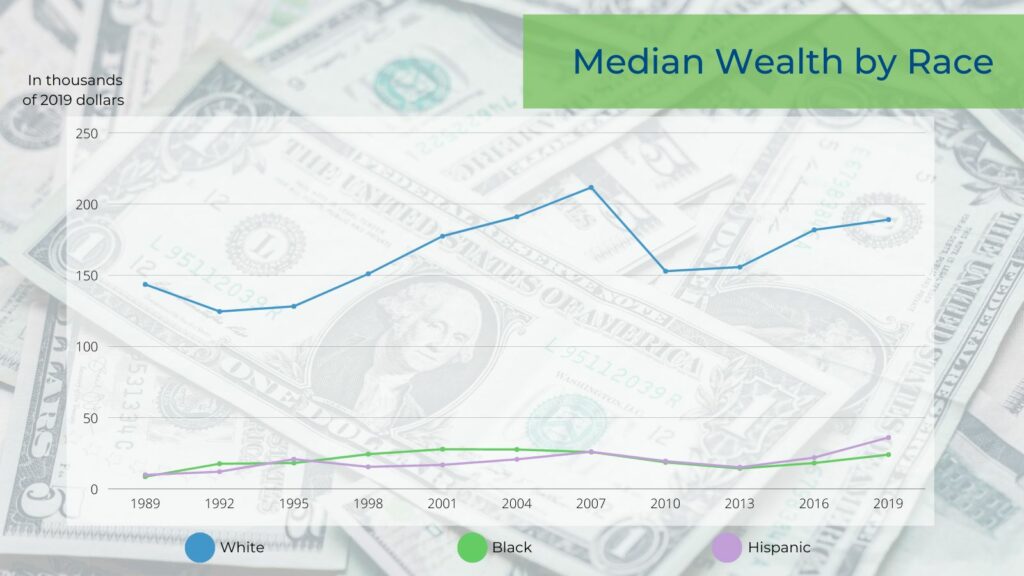

Additionally, the wealth gap between the top 10% and bottom 20% of income earners doubled, with gaps between the 40th to 60th, 60th to 80th, and 80th to 90th percentiles and the bottom 20% having also grown (by around 10%, 50%, and 45%, respectively). Currently, Black families’ median and mean wealth is less than 15 percent that of white families, a similar statistic as for Hispanic families.

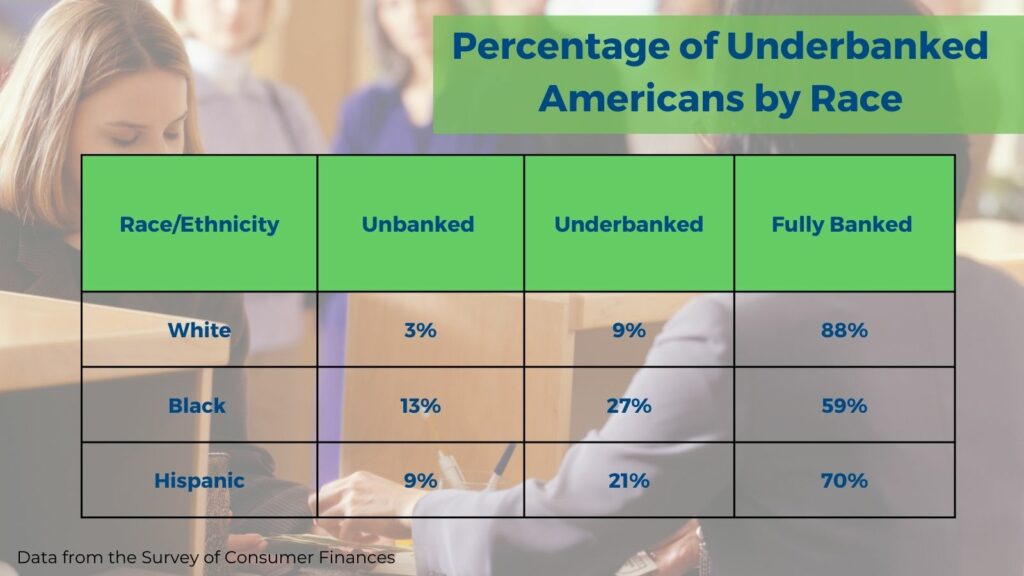

These shocking statistics are in part due to the lack of access to or provision of banking products and services to individuals and households in communities throughout our country.

Additionally, the banking industry has changed substantially since the last major update of the CRA rule in both the structure and operations of the banks themselves as well as consumer behaviors and preferences, underscoring the need to modernize the rule to account for online banking and other changes that were not foreseen when the CRA was originally passed.

Strengthening the CRA Rule through Accountability and Measurement

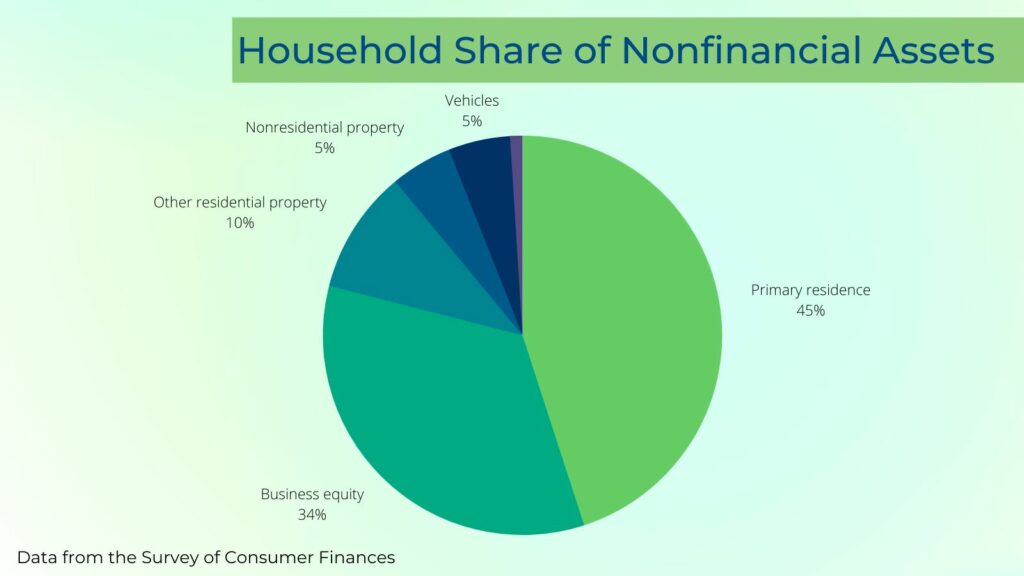

Home ownership has been shown to be the best way for the average household to build wealth over time. After all, mortgages allow borrowers to make at least a 5-to-1 leveraged investment in a unique asset that serves as both an investment and a place to live. In fact, households that own their home have 40 times more wealth than households that do not.

And small businesses are the backbone of many communities, allowing income and wealth to remain within a community rather than being siphoned out to a corporate headquarters in another region entirely. Local economic growth has been shown to be positively impacted by ownership of local small businesses. Additionally, one study has shown small businesses to be the source of 65% of job creation.

Therefore, banks must be held accountable in the CRA rule for their mortgage and small business lending to low- and moderate-income individuals and communities in a transparent, measurable, and meaningful way.

As has been proven repeatedly, if something is not concretely and granularly measured, monitored, and benchmarked in a meaningful way, it will never have its intended effect.

While the proposal has added a framework to make the final assessments around home, small business, and small farm lending more measurable, the framework lacks benchmark methodologies that are necessary to serve as a quantitative “sanity check” to the final assessment conclusions. Using a different methodology and taking a different perspective helps identify any shortcomings or special cases in which the primary methodology is under-performing. It is similar to ensuring there is diverse representation in a group so that multiple perspectives are considered. Therefore, the rule must include measurable, statistical benchmarks that would provide an alternative perspective and serve as a check on the validity of the non-statistical methodology of the proposed framework.

Also, a framework of “backstops” must be in place that set high-level minimum standards and prevent unreasonable outcomes. That is, backstops are necessary to put sensible limits on the conclusions.

Finally, the assessment of community development lending and investments should be made more quantitative and structured to have more measurability and transparency. The proposed methodology leaves too much to the discretion of the examination team and should incorporate thresholds that are tied directly to conclusions in the quantitative portion of the evaluation, similar to the retail lending test. Additionally, structure must be added to the qualitative portion of the evaluation, including how that structure maps to assessment conclusions.

Modernizing the CRA Rule by Accounting for Activity Outside of Physical Locations

The CRA rule is due for an update, in part, because of the significant technological shifts that have occurred since the last major update. It is now the case that not only can nearly every banking transaction be entered on a computer, they can also be entered on a smartphone. The most recent FDIC household survey of 2019 shows that 57% of households use either mobile or online banking as their primary method of account access. This has led to a disconnect (especially for online-based banks) between deposits that are sourced online, which can be from anywhere, and the CRA assessments, which are based on where banks have physical facilities.

The agencies propose to capture this change in business models with assessment areas that are based on concentrations of retail lending that occur away from physical locations. However, this methodology does not necessarily capture the “reinvestment” objective. Under the proposed framework, it is entirely possible banks (especially online-based banks) could obtain all their deposits from one set of areas but make all their loans in an entirely different set of areas. This disconnect could encourage banks to do exactly that and target their lending towards areas with lower proportions of LMI individuals.

To prevent such adverse incentives, the Agencies should base the additional assessment areas on concentrations of deposits rather than concentrations of loans. This would ensure conceptual consistency between the assessment areas that are based on physical locations and the new assessment areas outside of those. Basing on deposits would preserve the “reinvestment” aspect of the retail lending test assessment.

Enhancing Transparency and Public Trust

Historically, the Agencies have made CRA examination-related data available to the public. However, these data disclosures have been disjointed, being disseminated in numerous tables that are only available by a single cross section and are in several material ways incomplete, creating a high hurdle for any member of the public who attempts to perform analysis.

The Agencies must increase transparency by committing to publishing all available data annually for every bank, regardless of whether they are undergoing or have undergone a CRA-related examination with an easy-to-use interface that allows the public to dissect the data along any dimension. The interface also should include visual representations of the results and ability to download the resulting data set.