Banking regulators are required by law to identify risks and ensure they are mitigated before they materialize and cause bank failures, financial crashes, and economic contractions if not catastrophes. To do this, they are risk focused and content neutral. Put differently, regulators are indifferent as to where risks to the banking system arise; their focus is on risk identification regardless of where such risks might come from.

That is how to think about banking regulators and climate change: regulators are focused on the risk, not where the risk comes from. It’s like the threat from cyber: regulators don’t care that the risk to the banking system comes from cyber; they care about identifying the risk, understanding the risk, and ensuring that banks mitigate the risk. The same is true for the threat from climate, a serious, multi-faceted, and unprecedented threat to the banking system. Financial regulators and the institutions they supervise therefore must recognize the financial risks that climate events cause.

If regulators ignore climate change risks or exempt certain industries such as oil and gas from their risk analysis, they would violate their statutory duties to protect the stability of the nation’s financial system. Such an action—carving out an entire industry from regulators’ risk analysis—would be unprecedented, dangerous and, ultimately, extremely costly. Moreover, it would politicize neutral risk analysis by incentivizing other industries to lobby for their own special interest carve outs. The damage to the American people, the financial system, and our economy would be devastating, virtually guaranteeing more frequent and more damaging financial crises, crashes, and bailouts.

These inevitabilities are highlighted by recent actions taken by the insurance industry to limit their losses from climate events. Because the losses from climate events have so dramatically increased in frequency and severity, many insurance companies are becoming insolvent or withdrawing from states and areas that pose the most extreme climate-related risks. The result is uninsured and uninsurable residential and commercial real estate, as well as the full range of small, medium, and large businesses.

For example, the Guardian reported on July 15, 2023:

“After at least six insurers went insolvent in Florida last year, Farmers … became the latest to pull out of the Florida market, saying in a statement that the decision was based on risk exposure in the hurricane-prone state. Climate change is threatening the very existence of some parts of Florida.”

While this is tragic for homeowners and problematic for insurance companies, it is exponentially worse for banks and the financial system. That’s because insurance companies limiting their losses does not eliminate the losses altogether; it merely shifts them to others like banks which have very large portfolios of loans and other credit instruments to those now uninsured and uninsurable real estate and businesses. When the inevitable climate disasters occur, those exposures will quickly become burgeoning losses, almost certainly at levels more than sufficient to cause banks to collapse, and possibly ignite a credit contraction, precipitate contagion, and result in a banking crisis if not a financial crash.

The financial loss resulting from climate events is material and must not be ignored by financial regulators or banks.

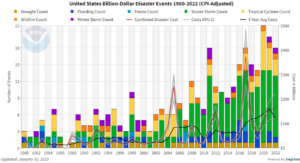

- The number of disasters and loss caused by climate events is increasing in the United States. In 2022, the U.S. experienced 18 separate weather and climate disasters costing at least $1 billion each, resulting in more than $165 billion in losses – in just one year. This puts 2022 into a three-way tie with 2017 and 2011 for the third-highest number of billion-dollar disasters in a calendar year, behind the 22 events in 2020 and the 20 events in 2021.

- The financial damages from disasters in 2022 of $165.1 billion were primarily driven by Hurricane Ian with $112.9 billion in damages, followed by the drought and heat wave that affected the western region of the U.S. and caused more than $20 billion in damages. In aggregate, billion-dollar disaster losses in the last 10 years (2013-2022) reached $1.1 trillion in the U.S.

- Importantly, these are conservative loss measures because they only include disasters with more than $1 billion in associated damages. Disasters that result in extreme damages to a local area should not be overlooked and could be incredibly meaningful to local communities and banks. Such smaller disasters cause damage to residential property, commercial property, agriculture, small businesses, and local infrastructure. It would be a grave and dangerous mistake for financial regulators to ignore these risks.

Source: NOAA National Centers for Environmental Information.

The loss resulting from climate events must be considered by financial regulators and banks alongside risks from other sources.

- The real threat comes from industry groups and others who are pushing regulators to ignore risks that result from climate-related factors. As Better Markets has said before, the fossil fuels industry and its allies are, in effect, insisting on a de facto prohibition on financial regulators from even looking at risks arising from climate.

- That is nothing less than asking financial regulators to pick winners and losers and engage in capital allocation decisions. Of course, if that industry’s campaign for special, undeserved treatment were successful, many other industries would quickly lobby to pressure financial regulators to exclude financial risks that arise from their activities.

- No one should be able to tell financial regulators what specific sources of risks to consider, identify, evaluate, or mitigate. Financial regulators are mandated to be neutral on the source of risk and include it for consideration regardless of where it comes from. To allow financial regulators to be constrained to only consider risks from specific sources but not others would threaten to cause another catastrophic financial crash.

- Banking regulators must take action to address the threat from climate change. In early 2023, Better Markets commented on a Federal Reserve proposal on principles for climate-related financial risk management for large institutions, supporting the need for consideration of the broad range of risks that climate change can pose, the need for metrics and scenario analysis to understand risks, and the need for explicitly integrating climate risk into existing risk management principles to make bank boards and senior management accountable.

The insurance industry has already recognized the gravity of financial risks stemming from climate events.

- To date, a key reason that banks have had limited losses from climate-related financial risks is because public programs and private insurance companies have absorbed most of those losses. Programs such as the National Flood Insurance Program (“NFIP”) which provides flood insurance for residential properties, and USDA’s Federal Crop Insurance, which protects farmers who are affected by natural disasters, shield banks from first-order losses in many climate-related disasters. Private insurance companies provide the same shield for homeowners and commercial properties and enterprises which will be are affected by fires or other natural disasters.

- Recently, however, more and more private insurance companies are realizing that climate risks have become so grave, consequential, and costly that they are abandoning entire states to limit their losses from climate events. These decisions harm consumers as insurance choices become limited and more costly if they are available at all. They also harm entire communities by eroding home values and increasing outmigration.

- For example, in Florida, many private insurers have left the state or scaled back new policies and renewals in response to severe weather events, increasing construction costs, and litigation risk. Floridians on average are paying more than $4,200 annually for home insurance premium, an increase of 42% compared with last year and well above the national average of $1,700.

- In response to a reduction in insurance availability for state residents, the Florida Legislature established Citizens Property Insurance Corporation (“Citizens”) in 2002. Citizens is a not-for-profit, tax exempt, state government entity that provides insurance to Florida homeowners who are unable to find insurance on the private market. Citizens is funded by policyholders’ premiums (which are much higher than the market rate from private insurers). Florida law requires Citizens to levy an assessment on Citizens and non-Citizens policyholders in the state if it experiences losses from particularly devastating storms.

- Given the already high and rapidly escalating costs of such insurance, it is unclear how much longer homeowners (many of them retirees) will be able to pay those premiums. Additionally, it is highly questionable if assessments to cover losses will be politically possible as climate related costs from disasters increase, particularly when larger and larger areas are crippled from climate events and people are out of work with no place to live.

- Another example is California, where State Farm and Allstate stopped issuing home insurance policies in 2023, in response to wildfire and flooding risk as well as rising construction costs.

- California also has a backup plan for when private insurance fails, called the “FAIR Plan,” which is a consortium of private insurers. It provides home insurance to Californians who have been denied insurance from private companies, also at much higher cost than private insurance. The number of new and renewed FAIR Plan policies nearly doubled between 2018 and 2021 (the latest data available).

- This plan suffers from many of the same weaknesses as Florida’s, raising serious questions about its sustainability and viability.

- For example, in Florida, many private insurers have left the state or scaled back new policies and renewals in response to severe weather events, increasing construction costs, and litigation risk. Floridians on average are paying more than $4,200 annually for home insurance premium, an increase of 42% compared with last year and well above the national average of $1,700.

- These actions highlight the very real and substantial threats that the known risks from future climate disasters pose to insurance companies. The same is true for banks and, indeed, they are worse for banks as insurance companies cut their losses due to the foreseeable and inevitable threats from climate, some of which get shifted to the banking system.

- It therefore cannot be denied that there are real and substantial risks from climate to the banking system and that regulators are mandated to identify and ensure that banks evaluate and mitigate such risks. To do otherwise would not only force regulators to violate the law but guarantee more frequent and more severe banking crises in the future.