It is not correct that recent changes to the Volcker Rule are “tweaks,” “nips,” “symbolic,” or otherwise insubstantial. It is also not correct that these changes merely “clarify,” “simplify” or “streamline” the prior rule. The changes are substantial, material, and consequential. They will enable and almost certainly result in significantly increased speculative trading by Wall Street’s biggest taxpayer-backed banks. After all, Wall Street did not spend enormous effort and money for more than nine years for changes that would not deliver them this outcome, their biggest victory since the 2008 financial crisis.

Based on a review of the new Volcker Rule, the FDIC fact sheet, Director Marty Gruenberg’s dissent, and comments made at the FDIC meeting, financial regulators have changed the original Volcker Rule in the following key ways:

First, the “Scope Loophole”: Dramatically Narrowing the Scope of Financial Instruments Covered. The new Volcker Rule substantially narrows the scope of financial instruments even covered by the Volcker Rule.

- No Fair Value Accounting Test: The new Volcker Rule does not include proposed definitional changes to the Trading Account (the Fair Value Accounting Test) that would have better ensured Wall Street’s banks are prohibited from engaging in statutorily covered prop trading positions.

- Flipping 60-Day Presumption: The new Volcker Rule instead changes the Trading Account definition to create a new presumption that financial instruments held more than 60 days are not speculative trades in violation of the Volcker Rule. This places the burden on bank supervisors to rebut the presumption and demonstrate otherwise, which will be extremely difficult, particularly in light of the reduced documentation the new rule permits banks to maintain and/or requires them to produce for supervisors.

- De Facto Elimination of Short-Term Trading Prong: The new Volcker Rule also effectively deletes the short-term trading intent prong of the Trading Account definition for banks subject to the market risk capital regulations. The new rule additionally permits banks not subject to the market risk capital rules to, in essence, opt out of the short-term trading intent prong of the Trading Account definition.

The market risk capital regulations require subject banking organizations to adjust capital requirements based on the market risks of trading positions. However, as defined for market risk capital purposes, these trading positions do not necessarily include all positions that might be held or traded for speculative purposes.

Through the combination of these three changes to the Trading Account definition, the new Volcker Rule substantially narrows the scope of the Volcker Rule and weakens a core pillar of the Dodd-Frank Act’s effort to have taxpayer-backed banks focus on providing credit to the productive economy, rather than engaging in speculative, high-risk trading activities that boost bonuses but risk impairing economic growth and financial stability.

|

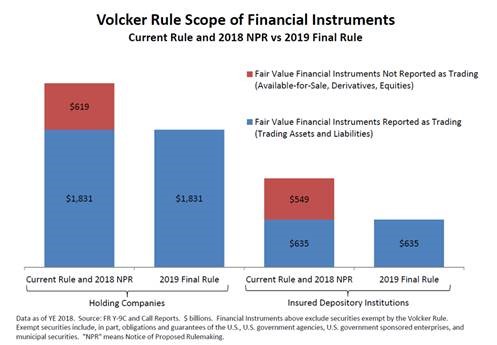

How much has the scope of the Volcker Rule changed relative to the 2018 proposal? |

FDIC Director Gruenberg laid out the analysis in his dissenting statement:

“[A]t the holding company level, about 25 percent of the financial instruments subject to the 2013 current rule and the 2018 [Notice of Proposed Rulemaking] would no longer be subject to the prohibition on proprietary trading . . . At the bank level, the final rule would exclude about 46 percent—nearly half—of financial instruments from the Volcker Rule that are subject under the 2013 current rule and the 2018 NPR.” (emphasis added)

Here is the chart Director Gruenberg’s dissent used to illustrate this significant change:

|

Key Questions to Ask the Wall Street Banks |

|

We believe the answer is “no,” which means many such positions may be outside of the revised Trading Account definition in newly scoped Volcker Rule. Remember, the new Volcker Rule, in essence, deletes the short-term trading intent prong of the Trading Account definition for banks subject to the market risk capital regulations (applicable to self-identified “trading” instruments). The new rule additionally permits banks not subject to the market risk capital rules to, in essence, opt out of the short-term trading intent prong of the Trading Account definition. Second, the “Presumption Loophole”: Self-Policing Presumption of Self-Compliance. The new Volcker Rule establishes a so-called “presumption of compliance” for certain market-making and underwriting activities. Those “presumptions” are a truly radical departure from longstanding supervisory practices and represent a return to the same failed industry self-policing policies and philosophies that prevailed before the 2008 financial crisis. |

|

The presumptions will now permit Wall Street’s largest banks to avoid or evade prop trading limits, because they permit, in effect, all trading activities conducted within risk limits established by the banks themselves. Thus, banks will set their own limits and then determine that they are in compliance with their own limits, which they are allowed to change (increase) without reporting that change to bank supervisors.

Traders at Wall Street’s banks will find it very easy to prop trade within such a self-established, self-referential, and self-policing regulatory framework.

Importantly, the use of risk limits for these purposes is conceptually non-sensical. Just as spending within credit card limits says nothing about what the money was spent on, trading within risk limits says nothing about the type of trading involved. Banks can and do speculate within risk limits.

|

How deferential are the new RENTD presumptions to the banks’ own judgments and self-policing? |

Extremely. In fact, it is hard to understand how a bank supervisor could effectively challenge any banks’ prop trading within a trading desk’s self-determined risk limit structure.

Here is select but key language in the final rule:

- “The agencies are adopting the presumption of compliance with the reasonably expected near term demand (RENTD) requirement for both the exemptions for underwriting and market making-related activities largely as proposed . . . [A] banking entity will be presumed to meet the RENTD requirements . . . with respect to the purchase or sale of a financial instrument if the banking entity has established and implements, maintains, and enforces the limits for the relevant trading desk.” 117.

- “[B]reaches of appropriately set limits may occur with a frequency that does not justify notifying the agencies for every single breach . . . Moreover, when a limit is breached or increased, the presumption of compliance with RENTD will continue to be available so long as the banking entity: (1) takes action as promptly as possible after a breach to bring the trading desk into compliance; and (2) follows established written authorization procedures.” 121.

A comprehensive analysis of the RENTD compliance program and the risk-limit basis for the “presumption of compliance” is beyond the scope of this fact sheet. But as the above makes clear, the new rule establishes a presumption of compliance with RENTD.

In other words, the new Volcker Rule requires compliance with RENTD but presumes firms are compliant with RENTD. Thus, the rule says, “You must do this,” but it also says, “I will presume you have already done it.” That guts the substantive statutory requirement, which will only exist in form.

|

Key Questions to Ask the Wall Street Banks |

|

|

|

Third, the “Hedging Loophole”: Non-Hedging Can Be Hedging. The new Volcker Rule will permit hedging that does not hedge—or what might be termed, “Humpty Dumpty Hedging”: a hedge is whatever the bank says it is [1] (which the new Volcker Rule will not then apply to). The new Volcker Rule, like the 2018 proposal, apparently eliminates the requirement that hedging activities “demonstrably” hedge anything. |

|

- Under the new Volcker Rule, banks do not need correlation analyses or any other specific analyses to show that hedging activities “demonstrably reduce” or “significantly mitigate” any actual risk. Banks merely need internal processes and procedures supposedly “designed” to reduce risks, even if they do not do so in reality.

In other words, Banks do not have to demonstrate that any hedge actually measurably reduces risks for the duration of the hedge, which violates the statutory requirement that hedging is permitted only if it is “risk mitigating.”

- Thus, other than generic policies and procedures, banks do not have to maintain specific documentation showing their actual hedges hedge and, therefore, it will be exceedingly difficult for regulators to properly review—much less police—the banks’ unilateral hedging decisions.

|

How deferential are the new hedging provisions to the banks’ own judgments and self-policing? |

Extremely. In fact, it is hard to understand how a bank supervisor could effectively challenge any banks’ prop trading disguised or even initiated as hedging.

Here is select but key language in the final rule:

- “[T]he agencies are removing the requirement that a correlation analysis be the type of analysis used to assess risk-mitigating hedging activities.” 148.

- “. . . [I]n some circumstances, it may be difficult for banking entities to know with sufficient certainty that a potential hedging activity . . . will continuously demonstrably reduce or significantly mitigate an identifiable risk after it is implemented . . . .” 150.

- “[T]he requirement that a hedge ‘demonstrably reduce’ or ‘significantly mitigate’ the identifiable risks could create uncertainty with respect to the hedge’s continued eligibility for the exemption . . . Therefore, the final rule removes the ‘demonstrably reduces or otherwise significantly mitigates’ specific risk requirement.” 150-151.

- “The final rule maintains the requirement that hedging activity . . . be designed to reduce or otherwise mitigate specific, identifiable risks . . . [but] the agencies do not find it necessary to require that the hedge ‘demonstrably reduce’ risk to the banking entity on an ongoing basis.” 151.

A comprehensive analysis of the new hedging loophole is beyond the scope of this fact sheet. But as the above makes clear, banks do not need correlation analyses or any other specific analyses to show that hedging activities “demonstrably reduce” or “significantly mitigate” any actual risk.

|

Key Questions to Ask the Wall Street Banks |

- Regarding your own risk management, if you don’t have to “demonstrate” that your hedging actually reduces risk, how do your internal risk, compliance, testing, and audit functions review, supervise, and test your so-called hedging activities to comply with your internal policies and procedures if not the law itself? Presumably for internal balance sheet and risk management, actual hedges must be required to demonstrably risk reduction? If so, why can’t that documentation be required and available to regulators?

- Would putting on a perfectly hedged bond position, then days later selling one leg of that position (leaving the other in place as a directional bet), violate the new Volcker Rule’s hedging requirements? If so, why or why not?

Final Thoughts on Wall Street’s Key Wins in the New Volcker Rule

These are just our initial impressions of the new Volcker Rule, which we will continue to review.

There is no genuine dispute that the new Volcker Rule will enable substantially more speculative proprietary trading. While this is a tremendous victory for Wall Street, it irresponsibly permits taxpayer-backed banks to engage in more socially useless and dangerous financial activities that do not support the productive economy or provide credit to create businesses, jobs and economic growth. These changes are short-sighted and once again privatize gains while socializing losses whereby the American people will again be forced to pay the bill for bailing out Wall Street’s reckless activities.

Better Markets is a non-profit, non-partisan, and independent organization founded in the wake of the 2008 financial crisis to promote the public interest in the financial markets, support the financial reform of Wall Street and make our financial system work for all Americans again. Better Markets works with allies – including many in finance – to promote pro-market, pro-business and pro-growth policies that help build a stronger, safer financial system that protects and promotes Americans’ jobs, savings, retirements and more. To learn more, visit www.bettermarkets.com.

For more information:

Contact: Christopher Elliott, 202-618-6433

Updated August 28, 2019

[1] “’When I use a word,’ Humpty Dumpty said, in a rather scornful tone, ‘it means just what I choose it to mean – neither more nor less.’ ‘The question is,’ said Alice, ‘whether you can make words mean so many different things.’ ‘The question is,’ said Humpty Dumpty, ‘which is to be master – that’s all.’” LEWIS CARROLL (Charles L. Dodgson), Through the Looking-Glass, chapter 6, p. 205 (1934). First published in 1872.