Introduction

Over the last several decades, Congress and the SEC have steadily expanded exemptions from the laws and regulations governing public securities offerings. This trend has diminished the vital role of the public markets, which offer a number of key benefits: mandatory public disclosure of material information by issuers; public trading venues such as exchanges that provide liquidity; and strong legal obligations and remedies for investors. Without corrective action, this growth in private markets at the expense of public markets will continue, and it will irreparably harm investors, market confidence, capital formation, and, ultimately, the economy as a whole.

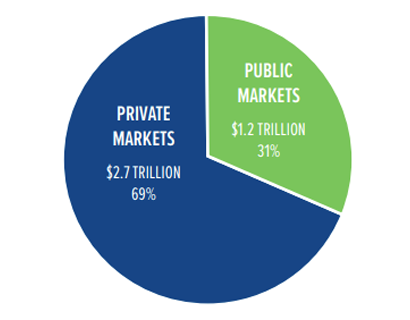

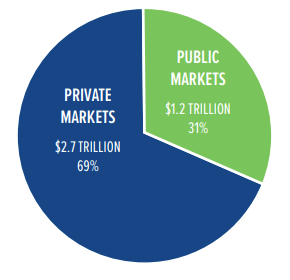

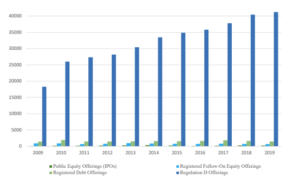

The present imbalance between private and public markets is clear. More than two-thirds of new capital raising in the U.S. securities markets occurs in private markets that are largely unregulated, opaque, and inaccessible to the public. The SEC estimates that in 2019, “registered offerings accounted for $1.2 trillion (30.8 percent) of new capital, compared to approximately $2.7 trillion (69.2 percent) . . . raised through exempt offerings.” Over the past decade, there has been a steady increase in Regulation D offerings,” the most relied upon exemption under the Securities Act. And state regulatory authorities have sounded similar alarms, emphasizing their experience with fraud and misconduct in the growing private markets.

The present imbalance between private and public markets is clear. More than two-thirds of new capital raising in the U.S. securities markets occurs in private markets that are largely unregulated, opaque, and inaccessible to the public. The SEC estimates that in 2019, “registered offerings accounted for $1.2 trillion (30.8 percent) of new capital, compared to approximately $2.7 trillion (69.2 percent) . . . raised through exempt offerings.” Over the past decade, there has been a steady increase in Regulation D offerings,” the most relied upon exemption under the Securities Act. And state regulatory authorities have sounded similar alarms, emphasizing their experience with fraud and misconduct in the growing private markets.

The private offering exemptions rest on false notions that they are “private” or “limited.”

The growth of private offerings, which dispense with the registration process, has rested largely on Securities Act section 4(a)(2), which provides that section 5’s registration requirements do not apply to “transactions by an issuer not involving any public offering.” Under this provision, the SEC instituted the Regulation D exemptive framework in 1982, which now represents the majority of private securities offerings. Securities Act section 3(b)(1) created another exemption, applicable to certain securities offerings of a “limited character” or having a “small amount involved.” Remarkably, Regulation D is only one element of a much broader (and still expanding) exemptive framework. The SEC now has an entire page on its website dedicated to summarizing the multiplicity of current exemptions. These other exemptions include Regulation A, Regulation Crowdfunding, Regulation S, Securities Act section 4(a)(2), and SEC Rule 144A.

The SEC has tied its own hands, so it has little information about private offerings.

With the growth of private markets, it is not just investors that live with a dearth of material information. The SEC is in the dark as well. This is because Form D filings are not subject to review and comment by SEC staff, unlike registration statements. It knows little about how many investors participate in these offerings, how much they invest, or how they fare. In essence, the SEC has taken a series of actions to expand the private markets with limited or no reliable information with which to reasonably judge the implications of its actions. This lack of data is associated not only with primary issuances but also with the absence of ongoing reporting obligations.

A classic example is the Form D filed by Theranos, which included only the most skeletal information about the company as it sought to raise $100 million in the private markets. The company was eventually embroiled in a huge scandal and its CEO was criminally prosecuted. A more recent example is the Form D filed by FTX, which also included minimal information about the company.

The public market framework has proven its merit, while exempt offerings pose major risks

The U.S. regulatory framework for public offerings is simple in one sense: It rests on the notion that investors can decide for themselves where to place their money at risk, provided they receive full and fair disclosure of all material information about a particular security before arriving at their own judgments. This system as led to broad, deep, and liquid capital markets with a worldwide reputation for integrity and strong oversight.

Consider one case exemplifying the benefits of robust disclosure that comes with public offerings: The 2019 lead-up to the We Company (parent of WeWork) IPO, a unicorn private company that had raised billions of dollars in private financings over its ten-year history. As it prepared for its IPO in 2019, it was required to disclose all material information in the registration documents it was required to file with the SEC. The ensuing public and investor scrutiny ultimately unearthed a variety of concerns about the company and its valuation. The result is well known: WeWork imploded; the CEO was ousted; there was a major retrenchment and restructuring of the company; and the IPO was withdrawn (although resurrected in 2021).

In sharp contrast, exempt offerings lack the many safeguards accompanying public offerings. First and foremost, they provide nowhere near the level of transparency about the venture or company soliciting funds—the information investors need to fairly evaluate the risks. The quality and reliability of information is also lacking, especially as it relates to financial statements. The list goes on, as exempt offerings are exceedingly difficult to price accurately, and investors’ ability to sell their investments is often severely limited, as they lack a robust secondary public market. And when investors have been misled, their remedies are far more limited relative to public offerings.

Steps the SEC should be taking to reverse this trend

The SEC has listed several proposed rules for consideration by the Commission in its Fall Agenda that could reevaluate the role exempt offerings play in our capital markets. They include amendments to Regulation D and improvements to Form D, the currently almost meaningless filing that accompanies offerings under rule 506 D; changes to the definition of shareholder of record that helps determine which companies must file periodic reports with the SEC about their operations and financial condition; and adjustments to the Rule 144 holding period, which governs the resale of restricted securities issued in private offerings. While the SEC can and should go further in reexamining its existing exempt offerings framework, these rulemakings represent positive steps.

A comprehensive analysis by SEC staff of both the benefits and the harms arising from its exempt offering framework, for instance, should provide an assessment of how the companies use and abuse the many exempt offerings available to raise money from investors. While certain exempt offerings may have been introduced into our securities legal framework for good reasons over the years, there is no question that the massive expansion and cumulative effect of these exemptions has created a patchwork of regulations that benefits companies wishing to receive the benefits of raising money from investors without offering adequate investor protections. While some aspects of the private offering framework can only be reformed through Congressional action, this is clearly fertile ground for further analysis, study, and where possible, rulemaking by the SEC.

The Accredited Investor standard also plays a critical role in investor protection

Despite the SEC’s clear pro-investor mandate that private offerings should be reserved for “those who are shown to be able to fend for themselves,” many wish to diminish the Accredited Investor standard, opening private offerings up to countless retail investors unfamiliar with their potentially devastating risks. Proposals include allowing anyone to invest in private offerings up to a percentage of their income or assets, or even allowing anyone to “self-certify” that they are sophisticated and understand the risks of investing even without full disclosure and other safeguards. While some claim that the Accredited Investor definition should be eliminated or loosened under the misleading rubric of democratizing finance, the reality is just the opposite. The definition should be strengthened, as Congress intended in the Dodd-Frank Act, to limit the investor harm that the often high-risk, opaque, and illiquid private offerings can inflict.

The income and net worth qualifications under the current Accredited Investor definition have remained the same in dollar amount since 1982—over 40 years. Meanwhile, inflation has substantially eroded the value of the dollar. Inflation over the past several decades has already dramatically expanded the number of people who qualify as Accredited Investors. Indeed, the number of Accredited Investors eligible to participate in the private markets today has increased 550% since 1983 and continues to rise. Rather than further erode this important investor protection, it is past time to update it. Section 413 of the Dodd-Frank Act demonstrates a clear congressional intent to protect investors, noting that subsequent adjustments to the definition of Accredited Investors must only be those deemed appropriate “for the protection of investors” and the public interest. Ultimately, the SEC should strengthen the Accredited Investor definition so that it better serves its dual purposes: ensuring that investors have the sophistication to understand the heightened risks that come with exempt offerings, and ensuring that they also have sufficient financial assets to absorb any losses they suffer, an all-too-common occurrence for those who put their money at risk in exempt offerings.

Conclusion

To be clear, the private securities markets have a legitimate and important role in capital formation. However, they must not be permitted to supplant public markets by facilitating regulatory arbitrage and avoidance of transparency measures, investor protections, and market safeguards in contravention of the fundamental purposes of the securities markets and laws. Yet expanding the dark, unregulated private markets at the expense of public markets threatens the integrity and vitality of our capital markets and ultimately the financial lifeblood of our economy. Balance must be restored, and that will require Congress and the SEC to stop enlarging the private markets and then begin scaling back those that are now in place.