By Shayna Olesiuk | Director of Banking Policy

Below is the introduction of the report. Read the full report here or click the button below.

Introduction

Californians have long feared “The Big One,” an extreme earthquake that would cause unimaginable loss and devastation in the state. However, the fires that have destroyed entire communities in Southern California in recent weeks suggest that wildfires are actually an even bigger and more material risk to local communities, banks, and society.

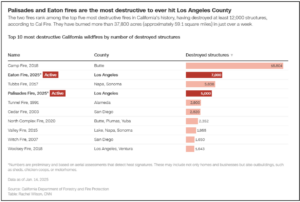

As of January 14, 2025, California state officials reported that 12,000 homes and other structures have been destroyed in the Palisades and Eaton fires combined (see Chart 1). Of course, the events and damage assessments are still ongoing, but experts currently estimate the cost of the fires to be between $250 billion and $275 billion, or about 6 percent of California’s $3.9 trillion GDP. These totals are, without question, enormous and add extreme financial pressure to families who are also facing devastating losses of life and livelihood. They also exceed the cost of damages left in the wake of Hurricane Helene, which last fall destroyed parts of multiple southeastern states Moreover, California’s fires add to a growing list of weather events that are increasingly endangering banks and the financial safety net across the county.

Chart 1

The situation in California has been complicated and exacerbated by a mass exodus of private insurance companies from the state in recent years. Large private insurers have dropped thousands of policies, leaving families exposed to disasters and forcing them to turn to state-run insurers-of-last-resort. These state-run “residual” insurance programs provide basic protections for families in need, but the coverage is typically much less robust than what is provided by a private insurance company and comes at a higher cost. This higher cost immediately strains families’ wallets, often forcing them to choose between groceries, medication, or other necessities and protection for their homes. However, after an extreme disaster or total loss as has been the case for thousands of Southern California families, even having insurance may be inadequate to support a complete home rebuild. In these cases, families are faced with the decision of whether to abandon their homes completely and stop making mortgage payments, essentially passing losses to banks and taxpayers. As we witnessed in 2008, when homeowners foreclose, banks are left holding the bag and shouldering the loss of unpaid loans. Losses also fall to taxpayers as Fannie Mae and Freddie Mac (“the GSEs”) hold significant shares of outstanding mortgages and if these loans go into default, the government and taxpayers will have to cover the costs.

Megabanks and community banks have large amounts of direct exposure to California real estate markets and are therefore highly vulnerable to natural disasters in the state. For example, large shares of Bank of America’s and Wells Fargo’s residential and commercial real estate mortgage loans are secured by homes and commercial property located in California. While the megabanks are unquestionably exposed to California, they are shielded by diversification and loans made in other states. However, 98 banks operate exclusively in California. The majority of these are community banks that do not have a safety net to lean on when disaster strikes. Even more concerning, 23 of these banks operate primarily or exclusively in Los Angeles County and are therefore even more acutely exposed to the devastation from the current wildfires. 12 of these are minority depository institutions, which means they specifically serve minority families with loans, deposits, and other banking products. Not only are the real estate loans vulnerable at these concentrated banks, but all loans—including consumer and business loans— at these banks are also at risk of default because of the thousands of individuals and small businesses that have lost everything. As explained earlier, these borrowers may have insufficient insurance coverage and simply choose to walk away.

A recent Senate Budget Committee report detailed how insurance industry risk will spread to the broader economy and financial system and result in more devastating outcomes than the 2008 Financial Crisis (“2008 Crash”):

According to one estimate, “climate change and the fight against it could wipe out 9% of the value of the world’s housing by 2050—which amounts to $25 [trillion].” Because the greatest source of wealth for most Americans is their homes, declining property values will erode household wealth. Any widescale decline in property values would thus present a systemic risk to the U.S. economy similar to what occurred during the 2007-2008 mortgage meltdown and ensuing global financial crisis. Indeed, the former chief economist for Freddie Mac has written with respect to a climate change-driven decline in coastal property values that “[t]he economic losses and social disruption may happen gradually, but they are likely to be greater in total than those experienced in the housing crisis and Great Recession.” The difference from 2008 is that the financial system and asset values could and did recover. The physical risks of climate change make a similar recovery unlikely: a home too endangered to insure will only become more endangered.

In the event that such a large-scale climate-driven decline in property values were to occur, the economic damage would not be confined to affected coastal communities. Across the United States, people would lose jobs, economic activity would contract, and retirement investments would lose value. It would be 2008 all over again, with the difference that—this time—the affected properties would never regain their value.

To date, actions by the Federal Reserve (“Fed”), the Federal Deposit Insurance Corporation (“FDIC”), and the Office of the Comptroller of the Currency (“OCC”) (collectively, the “Banking Regulators”) have been inadequate in responding to the climate-related financial risks that threaten our banks. Most recently, FDIC Vice Chair Travis Hill irresponsibly and wrongly dismissed the threat of these risks to banks, saying:

[T]here is no evidence such events pose an elevated safety and soundness or financial stability risk for banks. In fact, banks often benefit in the aftermath of such events as loan demand grows and recovery funds flow into the community.

At the same time, the Fed has refused to require banks to disclose climate risks and cooperate with international partners, even though these risks threaten banks in the same way as other risks that banks are required to disclose. Simply put, the American people deserve—and the financial system requires—regulators that hold banks accountable for all risks, regardless of the source. Instead, the Fed and other regulators have simply accepted the fact that the country’s largest banks are unaware of their risks, unable to measure their exposures to these risks, and lack the systems to monitor and manage these risks.