Below is the Introduction to the Report. Read the full Report here.

The failures of Silicon Valley Bank, Signature Bank, Silvergate Bank, and First Republic Bank—as well as the ongoing banking crisis—have galvanized attention to the risks and dangers posed by large U.S. banks. There is no doubt that the current crisis was exacerbated by the failure to properly regulate and supervise large banks (in these cases primarily the fault of the Federal Reserve and FDIC[1]), and to hold these banks accountable and demand rapid action to fix problems when they are being poorly and dangerously run.[2]

However, even before the latest failures and even before the Trump administration’s deregulation, the Fed and the other Banking Agencies have repeatedly failed to effectively enforce the rules and laws against large banks, including even the largest Wall Street banks. While those failures more directly contributed to the recent bank failures and fragility in the banking system, the lack of effective enforcement is also a significant contributing cause. When there is no appropriate punishment for breaking laws or failing to comply with financial safety rules, banks are not effectively deterred from engaging in illegal and unsafe behavior. That is particularly dangerous with respect to banks because they may then take on more risks, engage in more reckless activities, and create more dangers that heighten the threats they can pose to the economy, the financial system, and the well-being of the American people.

Given the outsized dangers posed by large banks, the importance of effective government oversight of these banks cannot be overstated. The failure of these banks—and the catastrophic results of earlier, failed approaches to the oversight of the largest banks—illustrate the damage caused by such banks when they are allowed to operate without financial regulators keeping them in check through strong oversight and enforcement supported by transparent public accountability.

A so-called “light touch” approach to banking oversight prior to the Global Financial Crisis (2008 Crash) contributed to the growth of predatory, reckless, and in some cases illegal behavior which resulted in the buildup of massive systemic risks that ignited that crisis.[3] That “hands off” approach by banking regulators was based largely on a mistaken yet widespread belief among many policymakers that the least regulation was the best because banks themselves had a strong interest in prioritizing their self-preservation over profits and that this, combined with the supposedly compelling powers of “market discipline” that would punish banks for engaging in bad or dangerously risky behavior (even if the activities were profitable in the short term), would serve to constrain the banks from engaging in overly dangerous activities.

It was believed that this combination would create appropriately strong incentives for large banks to manage themselves responsibly, without the need for stronger regulation and what was claimed to be burdensome, overly intrusive oversight by bank supervisors. As proved by the 2008 Crash, that “light touch” approach failed objectively and spectacularly, which resulted in the enactment of the Dodd-Frank Financial Reform and Consumer Protection Act (Dodd-Frank Act) and meaningful changes in oversight by the Banking Agencies responsible for regulating and supervising banks.

However, even before the failures of Silicon Valley Bank, Signature Bank, Silvergate Bank, and First Republic, large banks were regularly breaking the rules and laws and exhibiting routine and ongoing failures in basic risk management and consumer financial protection practices. Wells Fargo is the most egregious (and ongoing) example, but there are many others. For example, there were widespread basic risk management and control failures in both the JPMorgan “London Whale” losses in 2012 and the Goldman Sachs 1MDB crimes in 2012-2013 (which at least resulted in a modest, after-the-fact Fed sanction). The failure of the Archegos hedge fund in March of 2021 led the Fed to issue in December 2021 an unusual supervisory letter to “remind firms of the supervisory expectations” related to the fundamental management of well-known risks stemming from facilitating large market transactions.

The repetitive failure to comply with rules and laws at the biggest U.S. banks has been highlighted by Better Markets research as recently as May 2022. That Report detailed the lawbreaking by the six largest U.S. banks, and it indicates that the lawbreaking has actually increased since banks were re-regulated by Dodd-Frank. For example, in terms of legal actions against those banks (even if not in terms of the dollar amount of sanctions), they have jumped from 90 for unlawful conduct before the 2008 Crash to 232 since the 2008 Crash:

The Six Largest U.S. Banks – Collective RAP Sheet Highlights

Total Actions:430 | Total Sanctions: $198,558,675,333

| Time Period: | Pre-Crash | Crash-Related | Post-Crash |

| Actions | 90 | 108 | 232 |

| Sanctions | $14,358,799,785 | $156,283,675,000 | $27,916,200,548 |

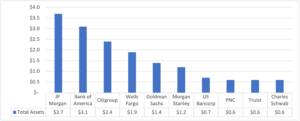

This is happening while the systemic risks posed by Wall Street’s largest banks have grown in recent years along with their size, scope, complexity, importance, and interconnectedness, and they remain too-big-to-fail (TBTF):

Largest Bank Holding Companies by Assets ($ Trillions)

Source: FR Y-9C report forms as of Q4 2022

Source: FR Y-9C report forms as of Q4 2022

This continues to be the case despite reforms put in place in 2010 following the 2008 Crash, including those in the Dodd-Frank Act, which had as a main objective addressing the dangers associated with TBTF banks and eliminating (or at the very least substantially reducing) the need for taxpayer-funded support when large banks get in trouble.

The dangers posed by these banks remain too great a threat to financial stability and the prosperity and livelihoods of the American people. In a period of economic and financial turmoil, when these banks are most likely to be struggling, the government will not allow them to fail, and they will be supported by taxpayer-funded programs and even bailouts. At the same time, their long history of dangerously poor management, as well as unethical and even illegal behavior, can give the public no confidence that large banks will operate safely and in compliance with rules and laws unless forced to through strong oversight by the Fed and the other Banking Agencies.

As has recently been demonstrated, these risks and dangers, however, are not limited to the very largest banks in the U.S., the so-called “GSIBs”: globally systemically important banks, which tend to get all the attention. As we have pointed out for years, similar risks arise from large (even if they are not the largest) banks, what we call “DSIBs”: domestically systemically important banks.[4] Unfortunately, since the Trump administration, the dangers and risks from these banks have been denied or ignored, as a result, they have been deregulated and under-supervised (see this Fact Sheet).[5] The gross deficiencies at and failures of the four large regional banks were the inevitable result of the weakening of oversight and are reminders that supervision, regulation and enforcement remain dangerously deficient for large banks.

Silicon Valley Bank will likely be remembered as a textbook case illustrating these failings. It has been revealed that the bank was subject to numerous supervisory findings including many at least six Matters Requiring Attention (MRA’s) and Matters Requiring Immediate Attention (“MRIA”) that had not been adequately addressed by the bank and which had not led to strong action taken by supervisors to require them to be addressed. It has also been publicly disclosed that the bank was subject to a confidential 4(m) agreement restriction, which can limit the activities of a bank or its ability to grow. These facts, including in particular those identified in confidential supervisory information that has been made public, all clearly demonstrate the need to strengthen the Fed’s supervision, regulation, and enforcement.[6]

[1] The oversight of banks operating in the U.S. is primarily the responsibility of the three banking regulatory agencies – The Federal Reserve (Fed), the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC), collectively referred to in this paper as “the Banking Agencies.”

[2] See Powell-Led Federal Reserve Deregulation Caused the Failure of Silicon Valley Bank and the 2023 Banking Crisis, Better Markets. (March 27, 2023), https://bettermarkets.org/wp-content/uploads/2023/03/BetterMarkets_FactSheet_Powell-Led_Fed_Eregulation_Caused_SVB_Failure_March-2023.pdf

[3] See The Cost of the Crisis – $20 Trillion and Counting, at 76-87, Better Markets. (July 2015) https://bettermarkets.org/wp-content/uploads/2021/07/Better-Markets-Cost-of-the-Crisis_1.pdf (“The causes of the financial crash and crisis will be debated for decades, if not longer. They were indeed multifaceted and complex. But make no mistake: The primary culprits were Wall Street’s too-big-to-fail financial institutions that engaged in an almost unprecedented binge of risk-taking, irresponsible lending, and, at times, massive illegal conduct.”).

[4] Scope and Definitions, Domestic Systemically Important Banks, Bank for International Settlements. (December 15, 2019), https://www.bis.org/basel_framework/chapter/SCO/50.htm

[5] See Powell-Led Federal Reserve Deregulation Caused the Failure of Silicon Valley Bank and the 2023 Banking Crisis, supra note 2.

[6] See Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank, Federal Reserve. (April 28, 2023), https://www.federalreserve.gov/publications/files/svb-review-20230428.pdf